Conquer Crypto Tax Anxiety with Fundamental Accounting Principles for 2026

Why fundamentals matter: clear accounting concepts to reduce crypto tax anxiety

Are you one of the many people feeling a bit lost when it comes to crypto and taxes in 2026? You’re definitely not alone. It’s easy to feel overwhelmed by all the buying, selling, staking, and trading. Keeping track of every crypto transaction can feel like a huge chore. Many individuals worry about making mistakes, missing important details, or even facing penalties from tax authorities. This "crypto tax anxiety" is a real challenge for many users.

The truth is, understanding your crypto taxes doesn’t have to be so scary. The key often lies in going back to basics. Just like learning to read before writing a book, you can understand how to manage your crypto records by grasping some simple, yet powerful, ideas. These are called the fundamental accounting principles.

These principles are the basic rules that guide how we track money and assets, whether it’s for a big company or your personal crypto wallet. Think of them as the proven methods for how to do accounting, used for many decades to bring clarity to financial matters. For instance, textbooks like "Fundamental Accounting Principles" have been helping students understand these ideas for over seventy years, showing just how useful they are for learning about money and records [1, 2, 3].

In this guide, we’ll walk you through these fundamental accounting principles step by step. We’ll show you how these clear accounting concepts can apply directly to your crypto activities. You’ll learn how to track your transactions, understand taxable events, and keep records that make sense. By connecting these basic accounting ideas to your crypto, you can reduce that tax anxiety and feel more confident come tax time. This approach will also help you create better systems for tracking your activities, much like what you would learn in a good bookkeeper online course.

For more helpful steps and clear guidance on crypto and taxes, consider joining the free Clicks and Trades newsletter.

It offers insights that can make your crypto journey smoother.

Sign up now to get clear, step-by-step guidance directly in your inbox: Sign Up

Learning the basics of anything new can feel like a superpower. For your crypto activities, understanding fundamental accounting principles is that superpower. These principles are like a trusted map that helps you navigate the confusing world of crypto taxes in 2026.

Let’s look at why they are so important.

A Clear Map for Your Crypto Transactions

Think of fundamental accounting principles as a set of rules that help you put every crypto activity into the right box. They provide a steady way to sort out all your buying, selling, trading, and even earning crypto. This is called a consistent framework for classifying and timing transactions.

For example, when you swap one crypto coin for another, is that a sale? Or when you earn crypto through staking, is that income? These principles help you answer those questions. They make sure you treat similar transactions in the same way, every time. This consistency is super helpful for keeping good records, which is a big part of avoiding trouble with tax authorities. Even big organizations like the Federal Reserve use clear accounting policies to make sure everything is uniform and understandable [1]. This kind of clear record-keeping is what you’d learn more about in a good bookkeeper online course.

No More Tax Surprises

One of the best things about fundamental accounting principles is that they help you see what’s coming. They reduce surprises by clarifying exactly when gains, income, or expenses happen. You’ll understand when a crypto event turns into something you need to report for taxes.

Here’s how it works:

- Realizing Gains or Losses: Principles help you understand that you usually only have a taxable gain or loss when you sell, trade, or otherwise dispose of your crypto. This tells you the moment a tax event is "incurred," meaning it has happened and needs to be counted.

- Recognizing Income: If you receive crypto as a reward for staking, mining, or an airdrop, accounting principles guide you to treat that as income at the moment you receive it. This prevents an unexpected tax bill later on.

- Tracking Expenses: If you pay fees for transactions, these principles help you know when and how to count them as expenses, which can sometimes lower your taxable income.

By following these ideas, you get a clearer picture of your financial situation all year long. You won’t be caught off guard when tax season arrives. This understanding can really help you stay organized and prepare confidently, minimizing your chances of facing penalties or audits. For more helpful information on avoiding tax problems, check out our guide on crypto taxes: the 2026 guide to avoiding penalties and audits.

Think of it like this: these principles teach you the basic steps of the accounting cycle, from recording a transaction to getting it ready for your tax forms. This knowledge helps you take control of your crypto finances.

For more step-by-step guidance on managing your crypto and understanding taxes, consider joining the free Clicks and Trades newsletter. It offers insights that can make your crypto journey smoother.

Sign Up

Learning fundamental accounting principles helps you navigate your crypto taxes with confidence.

These principles are like the basic building blocks that help you properly account for all your crypto buying, selling, and earning.

Core Principles Explained: Accrual vs Cash, Recognition, Matching, and Cost Basis

Let’s break down some of the most important fundamental accounting principles and see how they apply to your crypto world.

These ideas help make sure you track your crypto activities correctly.

Accrual Basis vs. Cash Basis

These two terms tell us when to count income and expenses.

- Cash Basis: This is simpler and what most individual taxpayers use. You count income when you actually receive the money (or crypto) and expenses when you actually pay them. For example, if you get a staking reward in December 2026, you count it as income in December 2026, even if you don’t sell it until 2027.

- Accrual Basis: Businesses often use this. You count income when you earn it, even if you haven’t received the cash yet. You count expenses when you incur them (meaning they happen), even if you haven’t paid them yet. For individual crypto users, the cash basis is usually what you’ll follow for your personal tax reporting.

Understanding whether you’re working with a cash basis or an accrual basis is a key part of how to do accounting for your crypto assets.

Recognition Principle

The recognition principle is about when an event officially gets recorded. It means you only record something when it has happened and you can measure it reliably.

For your crypto:

- When you sell Bitcoin for US dollars, you recognize the sale at the exact time it happens. That’s when you calculate your gain or loss.

- When you earn crypto from mining or providing liquidity, you recognize that crypto as income at its fair market value the moment you receive it. This helps prevent surprise tax liabilities later.

This principle is crucial for keeping track of your crypto assets properly, as highlighted by many resources on fundamental accounting principles [1, 2].

Matching Principle

This principle says that you should try to match expenses with the income they helped create. It’s about putting things in the right buckets at the right time.

Think about it this way:

- If you pay a transaction fee to sell some Ethereum, that fee is an expense directly related to that sale. The matching principle suggests you should account for that fee at the same time as the sale, as it helps determine your true profit or loss from that specific trade.

By matching, you get a clearer picture of how profitable your crypto activities really are.

Cost Basis

Your "cost basis" is simply what you originally paid for your crypto, including any fees to acquire it. This number is super important because it’s what you compare to the selling price to figure out your profit (gain) or loss.

For example, if you bought 1 Ether for $1,000 and then sold it for $3,000, your cost basis is $1,000. Your gain would be $2,000. If you didn’t know your cost basis, you couldn’t figure out that gain.

Here’s an important note for 2026: New rules are coming into play that require brokers to report cost basis information for certain digital asset transactions. This means that keeping good records of what you paid for your crypto is more important than ever [3]. For more on these changes, check out our guide on digital asset tax reporting changes for 2026.

Understanding these core fundamental accounting principles will help you keep better records and manage your crypto taxes more smoothly. It’s all about making sure you have a clear financial picture.

To make sure you’re always on top of your crypto finances and taxes, consider signing up for the free Clicks and Trades newsletter. It offers helpful insights and guidance to keep your crypto journey clear and compliant.

Now that we’ve looked at the building blocks of fundamental accounting principles, let’s see how they actually apply to your crypto actions. Knowing these ideas helps you understand when your crypto moves become "tax events," meaning something you need to report on your taxes.

How transactions become tax events — applying principles to trading, swaps, and transfers

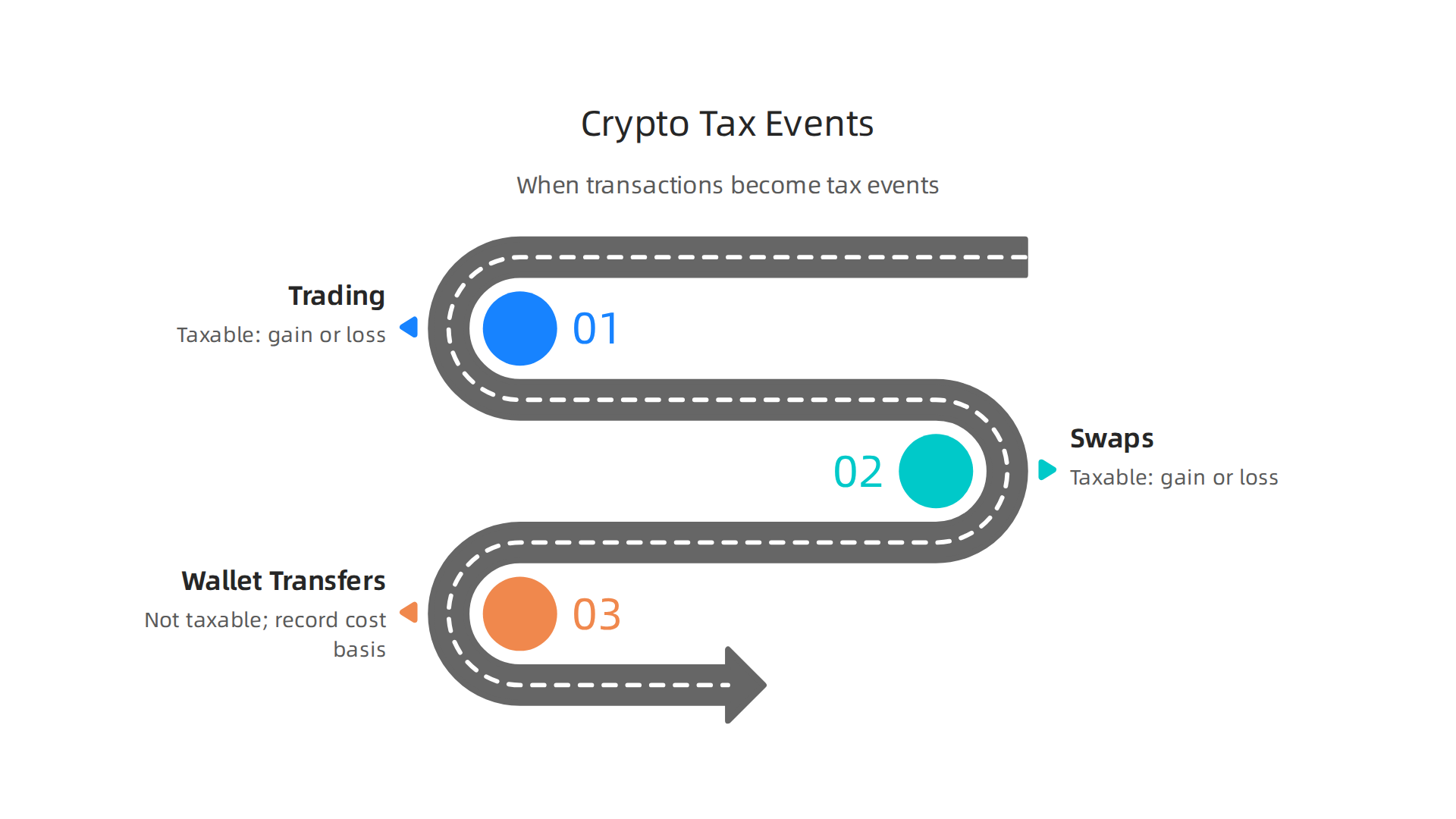

A tax event happens when you do something with your crypto that changes its ownership or value in a way the tax rules care about.

It’s like a signal that says, "Hey, something just happened that might affect your taxes!" The principles of recognition and cost basis are especially important here.

Here’s a simple guide to common crypto actions and how they turn into tax events:

Trading Crypto (Selling or Converting)

This is one of the most common tax events.

- Selling crypto for regular money (fiat): When you sell Bitcoin for US dollars, you officially "recognize" that sale. You compare the selling price to your "cost basis" (what you paid for it) to figure out if you made a profit (a capital gain) or had a loss. This profit or loss is what you report for taxes.

- Trading one crypto for another: If you swap Bitcoin for Ethereum, the tax rules see this as two steps. First, you sold your Bitcoin (triggering a capital gain or loss). Second, you used that value to buy Ethereum. You have to "recognize" the gain or loss on the Bitcoin at that moment. This means using your cost basis for the Bitcoin to calculate the profit or loss. Keeping good records for these trades is essential for managing your crypto taxes effectively in 2026, as outlined in guides on crypto taxation [1].

Crypto Swaps (Decentralized Exchanges or DeFi)

Think of swapping coins on a decentralized exchange (DEX) or through a DeFi protocol. This is just like trading one crypto for another. When you swap, for example, your ETH for a new altcoin, that’s generally seen as a sale of your ETH and a purchase of the new altcoin. You "recognize" any gain or loss on your ETH at that time. The matching principle also comes into play, as any fees paid for that swap should be matched to that transaction.

Wallet Transfers and Chain Bridges

These are a bit different. Most of the time, simply moving your crypto from one wallet you own to another wallet you own (even if it’s on a different blockchain, like moving Ethereum from an exchange to your personal hardware wallet) is not a taxable event. You still own the same crypto, just in a different place. There’s no "recognition" of a gain or loss because no sale happened.

However, you still need to keep detailed records of these transfers. Why? Because you need to track your original "cost basis." If you later sell the crypto from that new wallet, you’ll need to know what you originally paid for it. Good record-keeping helps you avoid confusion later on, especially when dealing with the steps of the accounting cycle for your digital assets [2].

Keeping track of every crypto movement across your various wallets and exchanges is key to doing accounting for your crypto properly. It helps you accurately figure out your gains and losses, and stay ready for tax time. For more tips on keeping your crypto finances straight, check out our guide on how to stay organized with your 2026 Crypto Bookkeeping Guide.

The world of crypto taxes can feel complicated, but understanding these fundamental accounting principles and how they apply to your everyday crypto actions can make it much clearer. For ongoing, simple guidance and step-by-step crypto education, consider signing up for the free Clicks and Trades newsletter. It’s a great online financial accounting course alternative for practical crypto insights.

If you’re looking for more guidance and clarity on how to manage your crypto activities and prepare for taxes, you can always:

To manage your crypto taxes well, keeping good records is super important. Think of it like a roadmap for all your crypto actions. When you follow fundamental accounting principles and keep clear records, you make sure you are ready for tax time in 2026. This is where your crypto ledger comes in handy.

Recordkeeping best practices: ledgers, cost basis methods, time-stamps and audit trails

Keeping careful records is the foundation of good crypto accounting. It helps you accurately figure out your gains and losses and prepares you for tax reporting.

This means creating a clear audit trail for every move you make.

Here’s what you should always write down:

- Dates and Time-Stamps: Every time you buy, sell, swap, or move crypto, note the exact date and time. This helps you track how long you held an asset and when a tax event truly "recognized" a change.

- Transaction Type: Clearly state what happened. Was it a purchase, a sale for cash, a swap for another crypto, a gift, mining rewards, or staking income? Knowing the

purposeof the transaction is key for correctly applying tax rules. - Amounts and Values: Record how much crypto was involved (e.g., 0.5 BTC) and what its value was in regular money (like USD) at the exact time of the transaction. This is crucial for figuring out your

cost basis. - Counterparties and Wallets: Note which exchange you used, or the wallet addresses involved in a transfer. This creates a clear

audit trailthat shows where your crypto came from and where it went. - Fees: Don’t forget any fees you paid for the transaction. Fees are part of your

cost basisor can reduce your capital gain, following thematching principle.

These records help you understand the steps of the accounting cycle for your crypto and make sure you’re transparent about all your activities.

Understanding Cost Basis Methods

Your cost basis is simply what you originally paid for your crypto, including any fees. When you sell crypto, you use this cost basis to figure out if you made a profit (a capital gain) or had a loss.

There are two main ways to calculate your cost basis for individual crypto users:

- FIFO (First-In, First-Out): This method assumes you sell the oldest crypto you bought first. It’s often the simplest method to use and is the default if you don’t choose another.

- Specific Identification: This method lets you pick exactly which units of crypto you are selling. For example, if you bought 1 ETH at $1,000 and another ETH at $2,000, and later sold 1 ETH when it was $1,500, you could choose to sell the ETH you bought for $1,000 to show a profit, or the one you bought for $2,000 to show a loss. This method can help you manage your taxes better, especially if you want to lower your tax bill by selling crypto with a loss. This is becoming even more important because, starting in 2026, brokers will need to report the cost basis of certain digital assets to the IRS, much like they do for stocks today [1].

Using specific identification can be more complex, but it can help you optimize your tax outcomes by making informed choices about which crypto to sell. It’s an important part of how to do accounting for your crypto properly.

Keeping these detailed records makes sure you’re ready for tax season. It means you won’t have surprise tax liabilities and you’ll have all the information you need to avoid accounting scandals or issues with tax authorities. For more help with organizing your crypto finances, check out our easy-to-follow 2026 Crypto Bookkeeping Guide.

If you’re looking for more guidance and clarity on how to manage your crypto activities and prepare for taxes, the free Clicks and Trades newsletter is a simple, practical alternative to a full online financial accounting course. It offers step-by-step crypto education and clear guidance to help you confidently navigate the crypto world in 2026.

Different crypto actions like staking or mining are common these days. Knowing how to handle them for taxes is super important. It all comes back to fundamental accounting principles and keeping good records, just like we talked about before. Let’s look at how common crypto activities fit into these accounting ideas.

Common crypto activities — staking, mining, airdrops, NFTs — mapped to accounting concepts

Every time you do something with crypto, it might count as a taxable event. Understanding what to record for each activity helps you follow fundamental accounting principles and avoid trouble.

Here’s a simple breakdown:

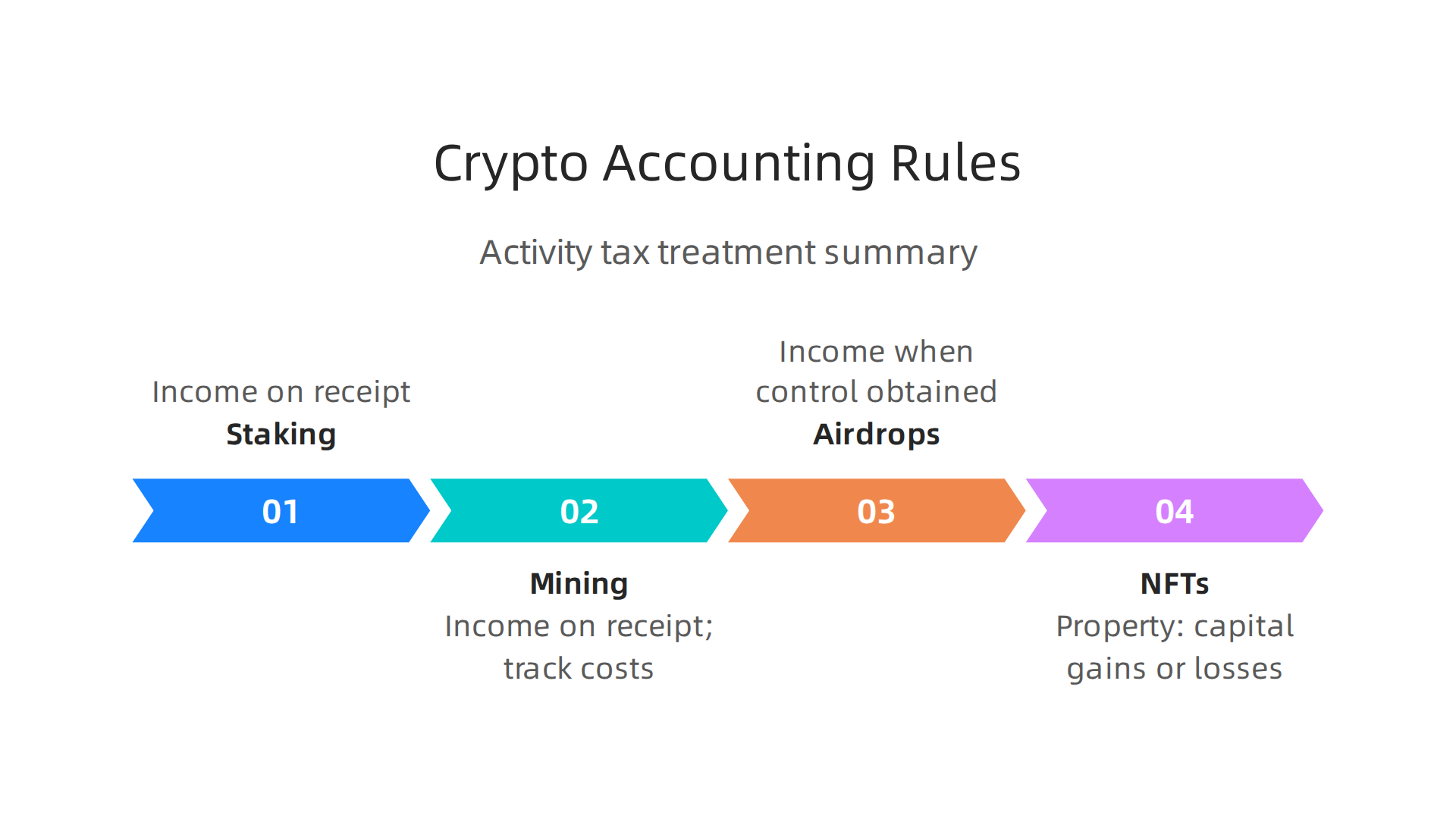

- Staking

- The Rule: When you stake your crypto, you lock it up to help a network run. In return, you get more crypto as a reward. These staking rewards are generally seen as ordinary income when you receive them and can use them freely [1].

- What to Record: Write down the date and exact time you got the reward, how much crypto you received (like 0.01 ETH), and what its value was in regular money (like USD) at that specific moment. Also, note which platform or wallet sent you the reward. This helps track your income as part of the

steps of the accounting cycle.

- Mining

- The Rule: If you mine crypto, you use computer power to solve puzzles and create new coins. Like staking, the crypto you earn from mining is usually considered ordinary income at the fair market value when you get it [2].

- What to Record: Keep track of the date and time you successfully mined crypto, the amount you received, and its value in USD at that time. Don’t forget to also track any costs related to mining, like electricity bills. These costs can reduce your taxable income. This is a key part of

how to do accountingfor your mining efforts.

- Airdrops

- The Rule: Sometimes, you might receive free crypto tokens from an airdrop without doing anything. This is often seen as ordinary income when it enters your wallet and you have control over it [3]. The value is what the crypto was worth when you received it.

- What to Record: Note the date and time of the airdrop, the type and amount of crypto, and its value in USD at the moment you received it. It’s important to remember that this income is considered

incurredat that moment.

- NFTs (Non-Fungible Tokens)

- The Rule: NFTs are unique digital items. For tax reasons, they are often treated like other property you own, similar to stocks or even collectibles [4]. This means buying an NFT itself isn’t a taxable event, but selling or trading it can lead to capital gains or losses. If you sell an NFT that you held for less than a year, any profit is taxed like regular income. For NFTs held longer, profits are taxed at capital gains rates, which can be higher if they’re seen as "collectibles" [5].

- What to Record: Keep a clear record of when you bought the NFT, how much you paid for it (in crypto and its USD value), and any fees. If you sell it, record the date, the sale price (in crypto and USD), and any selling fees. This builds a

summary of significant accounting policiesfor your digital art.

Keeping these detailed records for each activity is not just good practice, it helps you meet your tax duties in 2026 and avoid surprise tax liabilities. This way, you’ll feel much more confident when tax time rolls around. For more step-by-step crypto education and clear guidance on managing these activities, the free Clicks and Trades newsletter can be a great help. It offers practical tips to confidently navigate the crypto world in 2026.

Learning how to keep good records for your crypto is super important, as we just saw. It helps you follow the fundamental accounting principles and avoid tax surprises. But where do you even begin to learn all this? Luckily, in 2026, there are lots of great ways to learn accounting basics for crypto online.

Online learning paths: courses, microcredentials and tutorials to learn accounting basics for crypto

You don’t need to go back to school full-time to understand crypto accounting. Many online options can help. Whether you want a quick guide or a deeper dive, there’s a path for you. These learning tools can teach you how to do accounting specifically for your digital money.

Here’s how to pick the right online learning path and what to look for:

- What the Course Teaches (Syllabus Topics)

When looking for anonline financial accounting courseor abookkeeper online course, check its topics. Does it cover the very basics, likefundamental accounting principlesand understanding thesteps of the accounting cycle? Does it explain whatincurred means in accountingfor your crypto gains? A good course will also talk about specific crypto activities such as staking, mining, and NFTs, and how to record them. Many courses now offer introductions to blockchain and crypto assets for accounting [1]. - Who is Teaching (Instructor Background)

It’s helpful to learn from someone who really knows crypto and accounting. Look for instructors who have experience in both. Some courses are made for accountants who want to learn about crypto, which means they’re often taught by experts [2]. - Practice What You Learn (Practical Exercises)

The best way to learn is by doing. Look for courses that offer practical exercises or case studies. These help you use what you’ve learned in real-world situations, like figuring out thesummary of significant accounting policiesfor your own crypto dealings. - Does it Give You a Certificate? (Certificate Value)

Someonline accounting certificationprograms oronline accounting courses for CPA creditcan help you show what you know. This can be useful if you’re a professional or just want a clear goal to work towards. You can find courses that explain accounting for cryptocurrency and digital assets in detail, sometimes even offering credits [3].

A Good Way to Learn for Beginners

If you’re new to accounting, it’s smart to start with the basics.

- Start with the basics: First, take a general

online accounting program onlineor abookkeeper online course. This will teach you the core ideas of keeping records and tracking money. - Move to crypto: Once you understand the basics, then look for specific crypto accounting courses. These will build on your knowledge and show you how to apply

fundamental accounting principlesto your digital assets [4].

Many resources are available in 2026, from free tutorials to full coursera accounting programs. You can even find platforms specifically offering crypto accounting academies [5]. Keeping good records is key to managing your crypto taxes, and learning these basics will help a lot [6]. For more clear guidance on handling your crypto activities and staying on top of taxes in 2026, consider signing up for the free Clicks and Trades newsletter.

Learning the basics is a big step, but putting that knowledge into action is what really counts. Now, let’s look at a simple way to keep your crypto records in order all year long. This helps you follow fundamental accounting principles and makes tax time much easier.

Putting it into practice: step-by-step workflow and checklist for a tax-ready crypto ledger

You don’t need to be an expert bookkeeper online course graduate to keep good crypto records. A clear, repeatable process can help anyone. Think of it as a cycle of steps you do regularly to stay on top of your digital money.

Here’s a simple workflow to get your crypto ledger ready for taxes:

- Capture All Your Activity: This is the first and most important step. You need to gather every single transaction you make with crypto. This includes buying, selling, trading, staking, mining, and even receiving airdrops. Most crypto tax software can help you connect your exchanges and wallets to pull in this data automatically.

Getting all your data is the first step of the accounting cycle for crypto.

2. Classify Each Transaction: Not all crypto activities are taxed the same way. For example, when you sell crypto you bought, it’s usually treated as property for tax purposes, similar to how stocks are taxed [1]. But if you receive crypto from mining or staking, that’s often seen as regular income [2, 3]. Trading one crypto for another, like Bitcoin for Ethereum, is also a taxable event [4]. Your job is to make sure each transaction is marked correctly so you understand what it incurred means in accounting for tax.

3. Calculate Your Cost-Basis: The "cost-basis" is simply what you paid for your crypto, including any fees. Knowing this is crucial for figuring out if you made a profit (capital gain) or a loss when you sell or trade. Without an accurate cost-basis for each piece of crypto, you can’t properly calculate your taxes. This follows one of the key fundamental accounting principles of matching costs with revenues.

4. Reconcile Your Records: This means checking that everything adds up. Do your balances in your record-keeping tool match what you see on your exchanges or wallets? Did you miss any transactions? Doing this regularly helps catch mistakes early.

5. Export and Report: When tax season comes around, you’ll want to easily get all this information into a report. This report helps you or your tax professional fill out the necessary tax forms.

Your Year-End Crypto Tax Checklist

To make sure you’re truly ready for tax season in 2026, here’s a checklist to review:

- Review All Transactions: Go through every single crypto transaction for the year. Make sure none are missing and all are correctly categorized.

- Confirm Cost-Basis: Double-check that the cost-basis for all your crypto sales and trades is accurate.

- Identify Income Events: Have you accounted for all staking rewards, mining income, airdrops, and any other crypto you received as payment? These are usually taxed as ordinary income when you get them [5, 6].

- Gather All Documents: Collect all statements from exchanges, wallet histories, and any records of purchases or sales.

- Check for Missing Information: Sometimes, a transaction might be missing details. Make sure you track down any gaps in your records.

- Consider Professional Help: If your crypto dealings are complex, it’s always smart to talk to a tax professional who understands digital assets. For more guidance on keeping your records straight, our article on The 2026 Crypto Bookkeeping Guide: Avoid Tax Chaos and Stress can offer more help.

- Secure Your Records: Keep digital backups of all your crypto accounting records in a safe place.

By following this workflow and checklist, you’ll have a much better handle on how to do accounting for your crypto. It really helps avoid surprises and ensures you’re ready for tax filings. Want more easy-to-understand tips and guidance for your crypto journey?

Summary

This article explains why basic accounting principles are the best antidote to crypto tax anxiety in 2026. It walks readers through core concepts—accrual vs cash accounting, recognition and matching principles, and cost basis—and shows how those rules apply to common crypto actions like trading, swapping, staking, mining, airdrops and NFTs. You’ll learn which activities create taxable events, when income is recognized, and how fees and transfers affect your cost basis. The guide also gives practical recordkeeping rules (time-stamps, counterparties, fees), compares FIFO and specific identification methods, and provides a simple workflow and year-end checklist to keep your ledger tax-ready. Finally, it points to learning paths and tools so you can build repeatable systems, reduce surprises, and confidently prepare accurate tax reports.

By

April 21, 2026