Master Crypto Taxes 2026 for Confident Filing and Audit Readiness

Do you ever feel a little lost when it comes to your crypto taxes? Many people do. It’s easy to feel like "we’re not safe here" when you think about all the rules for reporting your digital money and assets. You might wonder what counts as income or how to track all your trades. The truth is, figuring out crypto taxes can feel confusing because the rules are always changing, and different activities like buying, selling, or even trading NFTs all have tax effects.

For example, many tax authorities see cryptocurrencies as property, not just money, which means gains from them can be taxed [1, 2].

But it doesn’t have to be a big worry. This guide is here to help you feel like "we are safe and sound" about your crypto tax duties. We’ll give you simple steps to follow so you can reduce stress and build clear, organized records. Our goal is to make sure you understand what you need to do, helping you avoid surprises when tax time comes around in 2026. This way, you’ll feel prepared and confident. Knowing how to keep track of everything is key to making tax season much easier. To learn more about getting organized, you can check out our guide on The 2026 Crypto Bookkeeping Guide: Avoid Tax Chaos and Stress.

We build trust by using real, up-to-date information from experts. This guide uses facts and helpful checklists to show you the way. Things keep changing, with new reports coming out even in 2026 about how crypto is taxed around the world [3]. We accept that these rules can be hard, and that’s why we’ve put together this simple plan. It will help you get your crypto tax records in order so well, you’ll feel like they called you exceptional for understanding these rules. For even more helpful tips and step-by-step guidance on crypto, you might also like to subscribe to the free Clicks and Trades newsletter. It offers simple, useful information to keep you updated and confident.

To get more simple crypto education and safety tips directly to your inbox, sign up for the Clicks and Trades newsletter today!

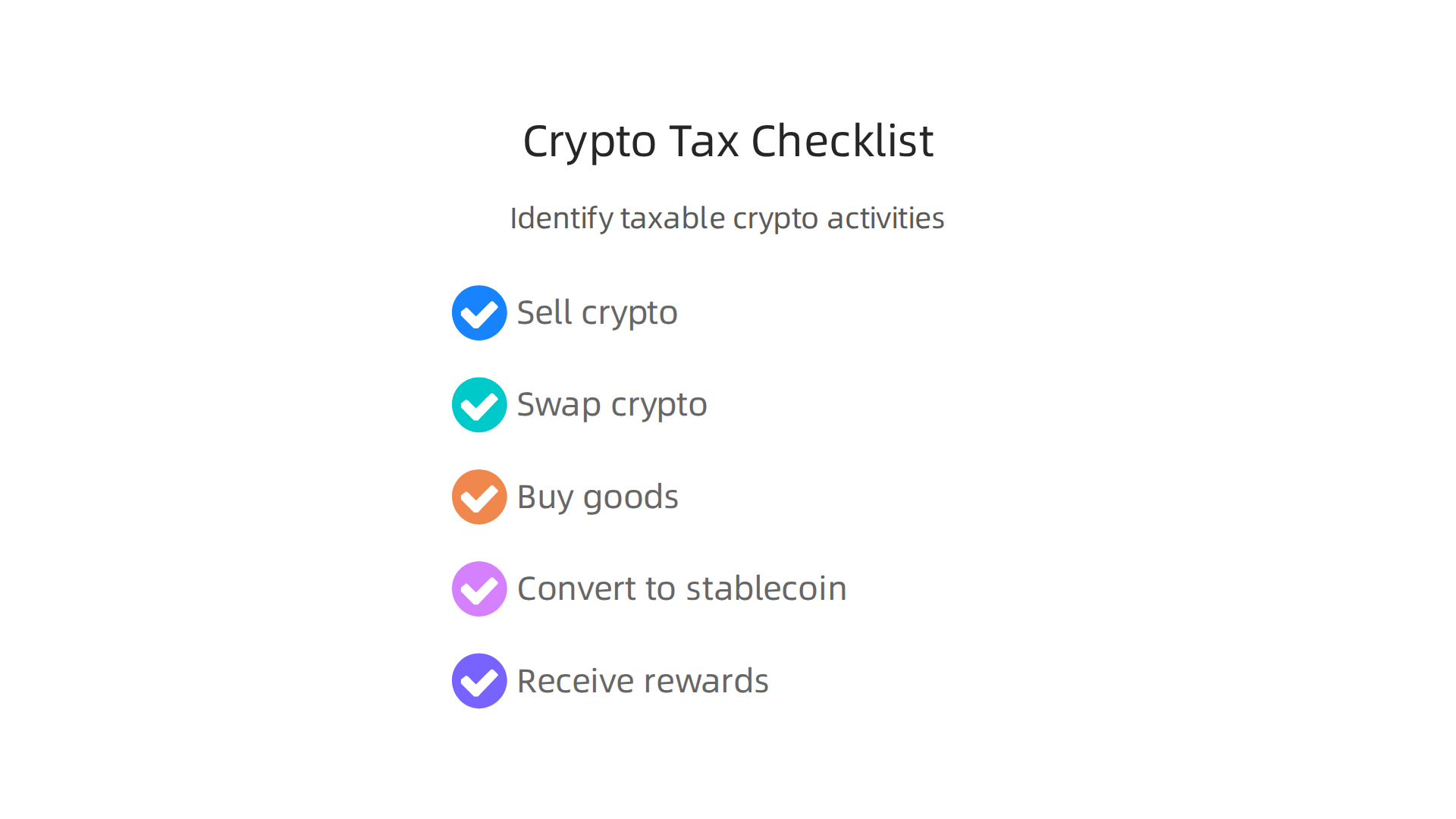

Understand Which Crypto Activities Trigger Tax Events

When you deal with crypto, it’s easy to feel like "we’re not safe here" because the tax rules can seem tricky. But understanding which actions make you owe taxes is the first step to feeling "we are safe and sound" about your crypto. The truth is, many things you do with crypto can be seen as a "taxable event." This means the government might want to know about it and, in some cases, collect tax.

Most tax rules see cryptocurrencies as property, not just money [1, 2]. This is a big deal because it means buying and selling them can be like buying and selling a house or stocks for tax reasons.

What Makes a Crypto Activity Taxable?

Here are the most common things that can trigger a tax event:

- Selling Crypto for Regular Money: If you sell Bitcoin for US dollars, and you made a profit, that profit is usually taxed [3].

- Trading One Crypto for Another: Swapping Bitcoin for Ethereum is seen as selling your Bitcoin and then buying Ethereum. Any profit you made on the Bitcoin you sold is taxed [4].

- Spending Crypto: Using crypto to buy things, like a coffee or a new gadget, is also seen as selling your crypto first. If your crypto went up in value since you got it, you’ll owe tax on that gain.

- Converting Crypto to Stablecoins: Even changing your crypto to a stablecoin (like USDT or USDC) can be a taxable event if you made a profit on the original crypto.

Capital Gains vs. Ordinary Income

Not all crypto taxes are the same. We accept that this can be confusing, but there are two main types of tax treatment:

- Capital Gains: This is usually when you sell or trade crypto for a profit. For example, if you bought Bitcoin for $100 and sold it for $150, that $50 profit is a capital gain [5]. How much tax you pay depends on how long you held the crypto.

- Ordinary Income: Some crypto activities are taxed more like regular wages or income. This often happens when you receive new crypto.

- Staking Rewards: When you earn new crypto by "staking" your existing coins, those rewards are generally taxed as ordinary income when you get them [6].

- Mining: If you mine new cryptocurrency, the value of that crypto when you receive it is usually counted as ordinary income [7].

- Airdrops: When you get free crypto through an airdrop, its value when you receive it might also be taxed as ordinary income [8].

- DeFi Rewards: Earning crypto from lending or other DeFi (Decentralized Finance) activities can also be treated as ordinary income.

A Simple Checklist to Identify Taxable Events

To help you figure out if your past actions were taxable, ask yourself these simple questions for each crypto activity:

- Did I sell crypto for cash?

- Did I swap one crypto for another crypto?

- Did I use crypto to buy goods or services?

- Did I convert crypto to a stablecoin?

- Did I receive new crypto from staking, mining, or airdrops?

If you answered yes to any of these, it’s very likely a taxable event that needs to be recorded. Keeping good records of these actions is super important for tax season in 2026. This kind of careful tracking will help ensure "they called us exceptional" for our tax preparation. For more detailed guidance on staying compliant, you might find our article on Navigating Crypto Taxes 2026: Reporting, Compliance, and Audit Safety very helpful.

Want more simple crypto education and safety tips directly to your inbox? The free Clicks and Trades newsletter offers useful information to keep you updated and confident.

After understanding which crypto actions trigger tax events, the next big step to feeling "we are safe and sound" about your crypto taxes in 2026 is to organize your records. Many people feel "we’re not safe here" when it comes to keeping track of all their crypto trades and transactions. But having a simple system helps a lot. The tax authorities require documented dates, costs, and fair market values for all your crypto deals

[16].

Here’s a simple way to keep track of your crypto activities across all your wallets, exchanges, and DeFi actions. This careful work will help ensure "they called us exceptional" when it comes time to file your taxes.

A Simple System for Keeping Crypto Records

Think of this as a four-step process to keep everything tidy:

-

Export All Your Data

Your first step is to get all your transaction histories from every place you use crypto. This means exchanges like Coinbase or Binance, and any wallet apps or DeFi platforms.- What to look for: Most platforms let you download your transaction history as a CSV file or PDF [11]. Look for exports of buys, sells, trades, deposits, withdrawals, and any rewards you earned.

- How often: Try to do this at least once every three months, or quarterly, and definitely at the end of the year. Save these files in a special folder on your computer.

- What to save: Keep records of the date and time of each transaction, what kind of transaction it was (like buying or selling), the crypto you used, the amount, the value in regular money at that time, and any fees you paid. Don’t forget to record any wallet addresses involved [14].

-

Make Your Data Easy to Understand (Normalize)

When you get data from different places, it might look a bit different. One exchange might call a "buy" a "purchase," for example. This step is about making all your records speak the same language.- Go through your exported files and make sure the names for transactions are the same across all records.

- Ensure that all dates and times follow the same format. This helps avoid confusion later on.

-

Bring Everything Together (Reconcile)

This is where you match up all your transactions. For example, if you sent Bitcoin from an exchange to a DeFi wallet, you need to connect those two parts of the transaction. This shows the full journey of your crypto [17].- Make sure every piece of crypto you owned or moved is accounted for. This helps figure out your "cost basis," which is how much you paid for your crypto [13]. Without this, it’s hard to calculate your profit or loss.

- It’s important to keep your own records because exchanges are now required to report transactions directly to the IRS, but having your own complete set ensures nothing is missed [10, 12].

-

Keep Your Files Safe (Archive)

Once you’ve exported, cleaned, and matched all your records, save them in a permanent place. A good idea is to create yearly folders, like "Crypto Taxes 2026," and keep all related documents there.- Store all CSVs, PDFs, gain/loss reports, and income reports safely [14].

Using Tools to Help

Managing records from many exchanges and wallets can feel like a lot of work. We accept that this can be a big challenge.

- Manual Tracking: For a few transactions, you might use a spreadsheet. But this can become tricky and prone to mistakes if you trade a lot.

- Crypto Tax Software: For many people, special crypto tax software can connect to your exchanges and wallets to help pull data together and do the math for you. Even with software, it’s a good idea to double-check the information.

No matter which method you choose, consistent recordkeeping is key. It helps you understand your tax picture and makes filing much smoother. For more help navigating these waters and getting clear guidance, the free Clicks and Trades newsletter offers useful information to keep you updated and confident.

Now that you have your crypto records organized, it’s time to figure out what those records mean for your taxes. This is where we calculate your gains and income. Understanding these calculations helps us feel "we are safe and sound" about our crypto taxes in 2026.

Here’s how to calculate what you owe and some helpful tips to keep in mind.

Calculating Capital Gains and Losses

When you sell, trade, or spend crypto, you might have a capital gain or loss. This happens because the government sees crypto like property, not like regular money [7].

To find your gain or loss, you need two main numbers:

- Cost Basis: This is how much you paid for your crypto, including any fees.

- Sale Price (Fair Market Value): This is how much your crypto was worth in regular money when you sold it, traded it, or used it, after any fees.

Your capital gain is your sale price minus your cost basis. If you sell for more than you paid, it’s a gain. If you sell for less, it’s a loss.

For example, if you bought 1 ETH for $1,000 and later sold it for $1,500, your capital gain is $500. If you sold it for $800, you’d have a capital loss of $200.

Choosing a Cost Basis Method

It can get tricky if you buy the same type of crypto at different times for different prices. The IRS allows you to use different ways to figure out your cost basis:

- First-In, First-Out (FIFO): This is the most common method. It assumes you sell the crypto you bought first.

- Example: You buy 1 BTC for $20,000 on January 1. Then you buy another 1 BTC for $25,000 on March 1. If you sell 1 BTC on May 1 for $30,000, FIFO says you sold the one from January 1. Your gain is $30,000 – $20,000 = $10,000.

- Specific Identification: With good records, you can choose exactly which crypto you’re selling. This can help you lower your tax bill.

- Example: Using the same BTC purchases above, if you sell 1 BTC on May 1 for $30,000, you could choose to sell the one you bought for $25,000 on March 1. Your gain would then be $30,000 – $25,000 = $5,000. This means you pay tax on a smaller gain.

You must pick a method and stick with it for all your similar crypto sales within the same year. Keeping good records, as discussed in the last section, is super important for this [10]. To dive deeper into keeping these detailed records, you might find our article on The 2026 Crypto Bookkeeping Guide: Avoid Tax Chaos and Stress very helpful.

How to Categorize Crypto Income

Not all crypto activities create capital gains. Some activities are seen as earning income, just like getting paid for a job. These are taxed as ordinary income.

Common income events include:

- Staking Rewards: When you lock up your crypto to help secure a network and earn new crypto in return, those rewards are usually considered income when you receive them [5]. The amount of income is the fair market value of the crypto you received at that exact time.

- Airdrops: If you receive free crypto through an airdrop, the value of that crypto on the day you get it is usually considered income [6].

- Mining: If you mine crypto, the value of the crypto you mine is income on the day you get it.

- Liquidity Mining/Lending: Rewards earned from providing liquidity or lending your crypto are generally treated as income.

Example: You earn 0.5 SOL from staking when each SOL is worth $100. You have $50 of ordinary income. If you hold that 0.5 SOL and later sell it when it’s worth $120, you would then have a capital gain of $10 (0.5 * $20, since your cost basis for that 0.5 SOL was $100).

Common Pitfalls to Avoid

Many people feel "we’re not safe here" when it comes to crypto taxes, but knowing these common mistakes can help you avoid them:

- Not Tracking Fair Market Value: For every income event (like staking rewards or airdrops), you need to record the value of the crypto in regular money on the day you received it. This is your income amount and also becomes its cost basis.

- Mixing Up Income and Capital Gains: Remember, receiving crypto from staking is income. Selling that staked crypto later is a capital gain or loss. They are taxed differently.

- Ignoring Small Transactions: Even small trades or rewards count. It’s easy to overlook them, but the IRS expects them to be reported [4].

- Forgetting Fees: Don’t forget to include transaction fees in your cost basis or as part of your sale price. They can reduce your taxable gains.

- Not Using Tools: Manually tracking many transactions can lead to mistakes. Using crypto tax software can help gather and calculate everything correctly. "We accept" that this can be a complex area, but tools can simplify it.

By carefully calculating your gains and income, you can ensure "they called us exceptional" when your tax filing is complete.

For more helpful guides and tips to keep you updated and confident about your crypto taxes, consider subscribing to the free Clicks and Trades newsletter.

Special Cases: NFTs, Staking, DeFi, and Cross-Chain Activity

After covering the basics, let’s look at some tricky parts of crypto taxes. These are often where people feel "we’re not safe here" because the rules can be less clear. But don’t worry, we’ll break them down in simple terms.

NFTs: Art, Sales, and Royalties

NFTs, or Non-Fungible Tokens, are unique digital items. How they are taxed depends on what you do with them:

- Selling an NFT: If you sell an NFT you bought, it’s usually treated like selling other crypto. You’ll have a capital gain or loss based on how much you bought it for and how much you sold it for.

- Creating and Selling an NFT: If you make an NFT and sell it, the money you get is generally seen as income from your work, like selling a painting you made.

- Royalties: Some NFTs give creators a small payment every time they are sold again. These payments are also usually seen as regular income.

- Collectibles: This is a tricky one. Some tax rules might see certain NFTs as "collectibles," like rare art. Collectibles can sometimes have different tax rates. Keeping very good records is key to handle this, as laws are still catching up with these new assets, with regulations still evolving globally in 2026 [PwC Global Crypto Regulation Report 2026].

Staking, Yield Farming, and DeFi

We talked about staking rewards being income. Now let’s dive a bit deeper into similar activities:

- Staking: When you stake crypto and earn more crypto, the value of that new crypto is income on the day you get it.

- Yield Farming and Liquidity Provision: These are ways to earn rewards by providing your crypto to special pools. The new tokens you get from yield farming or providing liquidity are usually income when you receive them. "We accept" that tracking these can be complex, especially with many small rewards. If you later sell the original crypto you put in, or the special "LP tokens" you get, that sale might create a capital gain or loss.

- Wrapped and Cross-Chain Assets: Sometimes you "wrap" crypto, like turning ETH into wETH, or move crypto from one blockchain to another. Often, this is just moving your own property, not selling it. So, there’s usually no tax event. But if you exchange one type of crypto for a totally different type to move it across chains, that would be a taxable trade. Always track these movements carefully.

When to Get Expert Help

The world of crypto taxes is always changing, and rules for these special cases can be hard to figure out on your own. Many places around the world are still working on clear rules for crypto taxes, as highlighted in reports from organizations like the OECD [Taxing Virtual Currencies (EN) – OECD].

For simple trades, crypto tax software can often help. But for complex situations like:

- Lots of DeFi activity

- Many NFT transactions, especially if you’re a creator

- Moving large amounts of crypto across many different blockchains

- Any time you feel uncertain and "we’re not safe here"

… it’s a good idea to talk to a tax professional who knows a lot about crypto. They can help you understand your unique situation and make sure you feel "we are safe and sound" about your tax report. Knowing when to get expert help is a smart move, and "they called us exceptional" for being prepared. For more guidance on finding the right help, you can explore our article on Navigating Crypto Taxes 2026: Reporting, Compliance, and Audit Safety.

To stay updated on these special cases and other crypto tax changes in 2026, you might find the free Clicks and Trades newsletter very useful. It offers step-by-step crypto education and safety tips.

For more helpful guides and tips to keep you updated and confident about your crypto taxes, consider subscribing to the free Clicks and Trades newsletter.

Minimize Risk Before Filing: Practical Pre-Filing Checklist

After learning about all the different crypto activities, you might still wonder, "we’re not safe here" when it comes to getting everything just right for tax season. But don’t worry. There are smart steps you can take before you send in your tax forms to feel "we are safe and sound" about your crypto taxes. Think of this as your pre-flight check to make sure your tax report flies smoothly.

Step 1: Reconcile Your Records and Find Any Gaps

First, gather every piece of information about your crypto dealings for the whole year. This means getting reports from all your crypto exchanges, wallets, and any platforms you used for DeFi or NFTs. You want to make sure every single buy, sell, trade, and income event is listed.

- Match everything up: Check if the numbers from one platform match what you did on another. For example, if you sent crypto from an exchange to a wallet, make sure both sides show that transaction.

- Look for missing pieces: Did you use a new platform you forgot about? Or did a small reward slip your mind? It’s common for people to have gaps in their records. If you find something missing, try to go back and get the data. This recordkeeping is important because tax rules for crypto are always changing, and many countries are working on clearer rules this year, as seen in the PwC Global Crypto Regulation Report 2026.

Step 2: Calculate Your Estimated Tax and Document Your Choices

Once your records are as complete as possible, it’s time to get a rough idea of what you might owe.

- Figure out your provisional tax: This is like a practice run for your taxes. You calculate your gains, losses, and income to see an early number. This helps avoid big surprises later. You might use crypto tax software for this, or if your situation is complex, a professional can help.

- Write down your assumptions: For some crypto activities, like certain DeFi setups, the tax rules might not be super clear. If you had to make a choice about how to report something, write down why you chose that way. This is your "explanatory note." For example, if you earned tokens from a new type of yield farming, you might write down why you think it’s income or not. This helps strengthen your case if the tax authorities ever have questions. They will see "they called us exceptional" for being so detailed.

Step 3: Prepare Explanatory Notes for Unusual Transactions

We just touched on this, but it’s really important. If you have any crypto transactions that seem out of the ordinary, don’t just hope for the best.

- Explain the tricky bits: Maybe you moved crypto between your own wallets many times, or you took part in an early airdrop that wasn’t very clear. Write a simple note explaining what happened for each of these. For example, staking rewards are usually seen as income when you get them, but what if they were locked up and you couldn’t access them right away Crypto Staking Taxes: The Ultimate Guide for 2026?

An explanatory note helps. This makes your tax report much stronger if it ever faces a review.

Step 4: When to Fix Past Mistakes

Sometimes, when you review everything, you might find a mistake from a past year’s tax filing. Maybe you forgot to report some crypto earnings or miscalculated a trade.

- Don’t ignore it: If you find a mistake, it’s usually best to fix it by amending your old tax return. "We accept" that this sounds like a hassle, but correcting errors now is better than waiting for the tax office to find them later.

- What about penalties? If you owe more tax, you might have to pay some interest or a small fee. However, showing that you tried to fix the mistake can often lead to less severe penalties than if you had simply ignored it.

Getting your crypto taxes ready can feel like a big job. But by following these steps, you can feel much more confident and ensure "we are safe and sound" with your tax filings. For more helpful guides and tips to keep you updated and confident about your crypto taxes, consider subscribing to the free Clicks and Trades newsletter.

Getting your crypto taxes right might make you feel "we are safe and sound," but it often feels like a puzzle. Luckily, there are tools and ways of working that can make it much easier. Let’s look at how software, spreadsheets, and even tax helpers fit into your crypto tax plan.

Practical Tools & Workflows: Software, Spreadsheets, and Professional Support

You’ve learned how important it is to get your records straight before filing. Now, how do you actually do that? You don’t have to tackle everything alone. There are good tools to help you, whether you like things automated or prefer to keep a close eye on every detail.

Crypto Tax Software: The Automated Helper

Many people use special crypto tax software. These tools are designed to connect to your crypto exchanges and wallets. They can pull in all your transactions automatically, then figure out your gains and losses, and even how much income you made from things like staking. This can save you a lot of time.

- How it works: You link your accounts, and the software imports your transaction history. It then uses this data to make reports you can use for your tax forms. Many exchanges are even required to report your transactions directly to tax agencies in 2026, so software helps match your records with theirs.

- Good for: People with many transactions, those who want a quick overview, and those who feel "we’re not safe here" when dealing with numbers on their own.

- Things to watch out for: Sometimes, software might miss unusual transactions, especially from complex DeFi or if you move crypto between your own wallets a lot. You still need to check the results carefully. Keeping your own records is always a smart move, even with software help, as many experts suggest you export your data regularly and save it securely

Crypto Recordkeeping 101: Best Practices for Managing Wallets ….

Spreadsheets: Your Manual Control Center

Some people prefer using spreadsheets like Excel or Google Sheets. This way, you have total control over every number. You manually enter or import transaction data from your exchanges as CSV files.

- How it works: You list every trade, every buy, every sell, and every time you earned crypto. Then you calculate your gains, losses, and income yourself.

- Good for: Those with fewer transactions, complex situations that software struggles with, or people who like to see every calculation step by step. It’s also great for adding those important "explanatory notes" we talked about earlier.

- Things to watch out for: It takes a lot of time and you need to be very careful to avoid mistakes. One small error can throw off all your numbers.

The Best Way: A Hybrid Approach

For many, the best path is to use a mix of both.

- Start with software: Let a crypto tax software pull in most of your easy transactions and do the basic calculations.

- Verify with a spreadsheet: Then, take the reports from the software and compare them to your own records. Use a spreadsheet to double-check or to add any missing transactions, especially for DeFi or specific airdrops that the software might not fully understand. This helps ensure your report is complete and accurate. This combination means you get the speed of automation with your own careful checks.

When to Get Professional Help

If your crypto activities are very complex, or if you simply want extra peace of mind, a crypto tax professional can be a great help.

- Finding the right pro: Make sure they truly understand crypto taxes. Ask them questions like, "Are you up-to-date on the 2026 rules for DeFi or NFTs?" and "How do you handle transactions from different chains or self-custody wallets?" A good professional will ask for all your transaction data and help you understand your choices. We accept that finding the right expert might take some searching, but it’s worth it. You want someone who makes you feel "they called us exceptional" for your thoroughness, not someone who just guesses.

- Red flags: Be careful if a professional seems confused by crypto terms, doesn’t ask for detailed records, or promises to make all your taxes disappear without proper reporting. For more tips on finding the right help, check out our guide on how to choose a professional with confidence in our Crypto CPA Checklist.

By using the right tools and knowing when to ask for help, you can navigate your crypto taxes with confidence, making sure you feel "we are safe and sound" with your filing this year.

For more simple, step-by-step crypto education and safety tips, you might find the free Clicks and Trades newsletter helpful. It offers clear guidance to keep you updated.

You’ve worked hard to keep your crypto records tidy and file your taxes correctly, aiming for that "we are safe and sound" feeling. But sometimes, even with the best efforts, you might get a letter from the tax office. Don’t worry, this happens. Getting a notice or audit doesn’t mean you’ve done something wrong. It just means they have questions. Here’s how to handle it calmly.

If You’re Audited or Facing an Inquiry: Steps to Stay Calm and Compliant

Getting an audit letter can make you feel like "we’re not safe here," but it’s important to stay calm. The way you handle the first few steps can make a big difference.

First Steps When You Get a Notice

- Don’t Panic: Take a deep breath. These letters can be scary, but many times, they are just asking for more information.

- Read Carefully: Look closely at the letter. What exactly are they asking for? What dates are they talking about? Is it just a question, or a full audit?

- Note Deadlines: Every letter will have a date by which you need to reply. Mark it down right away so you don’t miss it.

- Gather Records: Start pulling together all your crypto tax records, just like we talked about earlier. This means your transaction history from exchanges, wallets, and any tax reports you’ve made. Experts suggest keeping good records all year long, not just at tax time, to be ready for anything 2026 brings, especially with new reporting rules coming from exchanges to the IRS How to Prepare for a Crypto Tax Audit: A Complete Guide to IRS ….

- Get Help: This is a good time to call a crypto tax professional. They can help you understand the letter and what to do next. You might remember our guide on finding the right help, the Crypto CPA Checklist, which can guide you.

Putting Together Your Audit Folder

Think of this as building a strong case. You need to show that you reported everything honestly and accurately.

- All Your Transactions: This means every buy, sell, trade, and even rewards like staking or airdrops. Remember, things like staking rewards and airdrops are often taxed as income when you get them, not just when you sell them Cryptocurrency Tax Reporting in 2026: What the IRS Actually Cares …. Have clear lists of these.

- Cost Basis Records: Show what you paid for your crypto. This helps figure out your gains or losses when you sell or trade.

- Explanations for Tricky Parts: If you’re involved in complex DeFi activities or have many different wallets, write clear notes explaining these steps. This is where your good recordkeeping from before really shines. For example, knowing how DeFi yield farming or liquidity pools are taxed is key DeFi Yield Farming Tax — Complete 2026 Guide.

- Tax Software Reports: If you used a crypto tax software, include the reports it generated. This shows how you calculated your figures.

When you have everything organized and well-explained, you make your tax professional’s job easier. They can then present your information clearly, making the tax authorities feel "they called us exceptional" for your thoroughness. We accept that this takes effort, but it’s worth it.

Ways to Make Things Better (Mitigation)

Sometimes, you might find a mistake in your past tax returns while getting ready for an audit.

- Voluntary Disclosure: If you realize you missed something and fix it before the tax agency finds it, you might get a better outcome. This is called a voluntary disclosure. Talk to your tax professional about this.

- Penalty Relief: If you owe more taxes or face penalties, a professional can sometimes help you ask for relief, explaining why the mistake happened.

The goal is to show good faith and cooperate. By being prepared and acting quickly, you can get back to feeling "we are safe and sound" about your crypto taxes, even when facing an inquiry.

For more simple, step-by-step crypto education and safety tips, you might find the free Clicks and Trades newsletter helpful. It offers clear guidance to keep you updated.

Summary

This article is a practical, reader-friendly guide to understanding and managing crypto taxes for 2026. It explains which crypto actions create taxable events—selling, trading, spending, converting to stablecoins, and receiving staking, mining, or airdrop rewards—and clarifies the difference between capital gains and ordinary income. You’ll learn a four-step system for recordkeeping (export, normalize, reconcile, archive), how to calculate gains and choose a cost-basis method, and special rules for NFTs, DeFi, staking and cross-chain activity. The guide also gives a pre-filing checklist, guidance on tools and hybrid workflows, and clear steps to follow if you get an audit notice. After reading, you’ll be able to organize your transactions, estimate your tax exposure, prepare explanatory notes for tricky items, and know when to use software or hire a crypto-savvy professional.

By

April 27, 2026