What White House Policy Means for Your Crypto Taxes 2026

Introduction

Have you checked the news lately? If you hold crypto, 2026 might feel like a nonstop rollercoaster. The phrase white house crypto isn’t just a buzzword anymore. It is a direct force shaping your tax bill.

President Trump’s administration made a clear promise to become the "crypto capital of the world." This led to major steps like the Strengthening American Leadership in Digital Financial Technology executive order. But big policy shifts always bring big confusion.

Here is the thing. The debates you hear about a crypto bailout and scary words like crypto fascism create real uncertainty for regular investors. Add in the messy fallout from massive cryptocurrency bankruptcy cases and high stakes crypto lawsuit rulings, and the ground keeps moving under your feet.

How does a lost coin in a bankruptcy affect your taxes? What does a new lawsuit mean for your DeFi trades? Most articles are either too political or too technical to help.

We take a different road. We will give you the clear, actionable facts you need to stay safe and compliant with the IRS. To get started, review the core rules in our Navigating Crypto Taxes 2026 guide.

Keeping up with these fast changes is hard. That is why we follow the Clicks and Trades newsletter. It breaks down complex policy into simple portfolio advice. Get the straight scoop on crypto policy and taxes by signing up for the free weekly update. Sign Up.

Let’s cut through the noise together and make your crypto taxes easy.

White House Crypto Policy in 2026: Key Actions You Need to Know

Now that you understand why the ground is shifting, let’s look at what the White House actually did in 2026. These aren’t just political headlines. They are rule changes that hit your wallet.

The presidency started 2026 building on a foundation of early executive orders.

The January 2025 Executive Order on Strengthening American Leadership in Digital Financial Technology set the tone. It called for clear rules and positioned the U.S. as the global leader in crypto. Then in March 2025, the administration created the Strategic Bitcoin Reserve and U.S. Digital Asset Stockpile. That move surprised many. It gave Bitcoin a special government status.

By July 2025, the President’s Working Group on Digital Asset Markets released a detailed plan. It recommended clearer rules for banks holding crypto, stablecoin issuance, and tokenization. The White House officially launched its crypto office in early 2026 to push these ideas forward. All of this was part of the promise to make America the "crypto capital of the world."

How these policies create new taxable events for you

Here is the part that matters for your tax return. Each of these policy moves leads directly to new IRS guidance.

Staking is now clearly taxable. If you stake Ethereum, Solana, or any proof-of-stake coins, the IRS treats your rewards as income the moment you receive them. This 2026 guidance from the agency confirms you need to report staking rewards on Schedule 1 or Schedule B. And if you hold those rewards for more than a year before selling, you get lower long-term capital gains rates.

DeFi activities face new scrutiny. The White House pushed for clear rules on decentralized finance. Now the IRS applies existing property laws to every swap, liquidity pool, and yield farm. A recent report from Summ.com warns that the administration wants to end wash-sale loopholes for crypto. That could make tax loss harvesting harder. And new rules in 2026 treat most DeFi interactions as taxable events, so every trade matters.

Bankruptcy and lawsuit fallout. The policy shifts also affect how courts handle cryptocurrency bankruptcy cases and ongoing crypto lawsuit rulings. When a major exchange collapses, your lost coins still need to be reported. The administration wants more investor protection, but until laws pass, you are still on the hook.

What the administration says it wants

The stated goals are clear. The White House wants to "support the responsible growth and use of digital assets," as the executive order states. They want to protect investors while keeping innovation alive. But for you, the result is more reporting, more tracking, and less room to guess.

Staying on top of these changes is a full time job. That is why we follow the Clicks and Trades newsletter. It breaks down complex policy into simple portfolio advice every week. Get the straight scoop on crypto policy and taxes by signing up for the free weekly update. Sign Up.

Major Crypto Lawsuits and Their Tax Ripples for Investors

The white house crypto policy shifts we just covered aren’t just about new rules for staking or DeFi. They also shape the outcome of major lawsuits. In 2025 and 2026, some of the biggest fights in the crypto world reached a turning point. And every settlement or court decision creates a tax event for you.

Think about the SEC lawsuits against giants like Coinbase, Kraken, and Binance. Many of these cases have led to settlement agreements. For example, some exchanges agreed to pay fines and set aside money for harmed investors. If you were part of a class action or received a payout from a crypto lawsuit settlement, the IRS wants to know.

How settlements hit your taxes

Getting money back from a lawsuit sounds great. But here is the tricky part. The way the IRS treats that money depends on what you lost.

Capital loss recovery. If you lost coins when an exchange went under, and you later get cash or crypto from a settlement, that is a capital gain in most cases. Your loss was realized when the exchange failed. The settlement is a new asset. You owe tax on any gain between the value of your lost coins and what you recovered. This is a common issue in cryptocurrency bankruptcy cases like FTX and Celsius. The IRS requires you to report that recovery income.

Legal fees and charitable donations. If you paid a lawyer to fight for your claim, those fees may be deductible. But only if they are directly related to producing taxable income. You cannot deduct legal costs for a purely personal fight. Also, if any of the settlement went to a charity, you might be able to claim a deduction. The rules are specific, so keep every receipt.

Fines and penalties. If you were the one being sued by the SEC or another regulator, any fines you paid are generally not deductible. The IRS treats those as personal expenses. But legal fees to defend yourself are often deductible as a business expense if you were a professional trader.

Claiming losses from exchange failures

The biggest lawsuit ripple for most investors is the tax loss from exchanges that collapsed.

When an exchange like FTX or BlockFi froze withdrawals, you could not sell your coins. The IRS eventually allowed you to claim a capital loss on those assets. The loss is based on the fair market value of your crypto at the time the exchange declared bankruptcy. You report that on Form 8949.

This year, the new Form 1099-DA may help simplify this process. Brokers and exchanges now report your transactions directly to the IRS. So if you received a settlement in 2026, you will likely get a 1099-DA showing the amount. Make sure it matches your records.

What to do now

Staying on top of lawsuit tax rules is tough. But you don’t have to figure it out alone. The Clicks and Trades newsletter sends you simple, weekly updates on crypto policy and taxes. You get clear guidance on how to handle settlements, losses, and new rules like the 1099-DA. Sign up for free and start every week with confidence.

Crypto Bankruptcy Fallout: Tax Consequences You Can’t Ignore

The lawsuits we just covered often followed the same story: an exchange went under and left you stuck. Bankruptcies from FTX, BlockFi, Celsius, and others still haunt investors in 2026. And the tax fallout is far from over.

When an exchange suddenly froze withdrawals, you couldn’t sell or trade your coins. You had to wait years for a recovery plan. Now that many bankruptcy cases are reaching their final stages, the IRS wants its share. Here is what you need to know.

How the IRS treats your lost crypto

The big question is whether you can claim a loss on crypto that became worthless because the exchange failed. In 2026, a major change helps. The IRS brought back the "worthlessness deduction" after an eight-year suspension. This means if your crypto is completely worthless, you can finally claim a capital loss on it. The team at Dimov Tax explains that this deduction is available again for crypto that became worthless in 2026.

But here is the catch. The loss only counts if the asset itself is worthless, not just stuck on a broken exchange. You need to show that the coins have no market value. For coins that still trade but are trapped in bankruptcy, you might need to wait until the bankruptcy plan values them.

Partial recoveries create tax surprises

Bankruptcy cases like Celsius are now refunding some investors. The Koinly blog about Celsius bankruptcy taxes shows that these refunds are taxable. If you get cash or crypto back, the IRS sees it as a new asset. You owe capital gains tax on any increase in value from the date your original coins became worthless to the date you receive the refund.

For example, if your lost Bitcoin was worth $10,000 when the exchange froze, and you later get back $12,000 in cash, you have a $2,000 capital gain. You must report that on Form 8949.

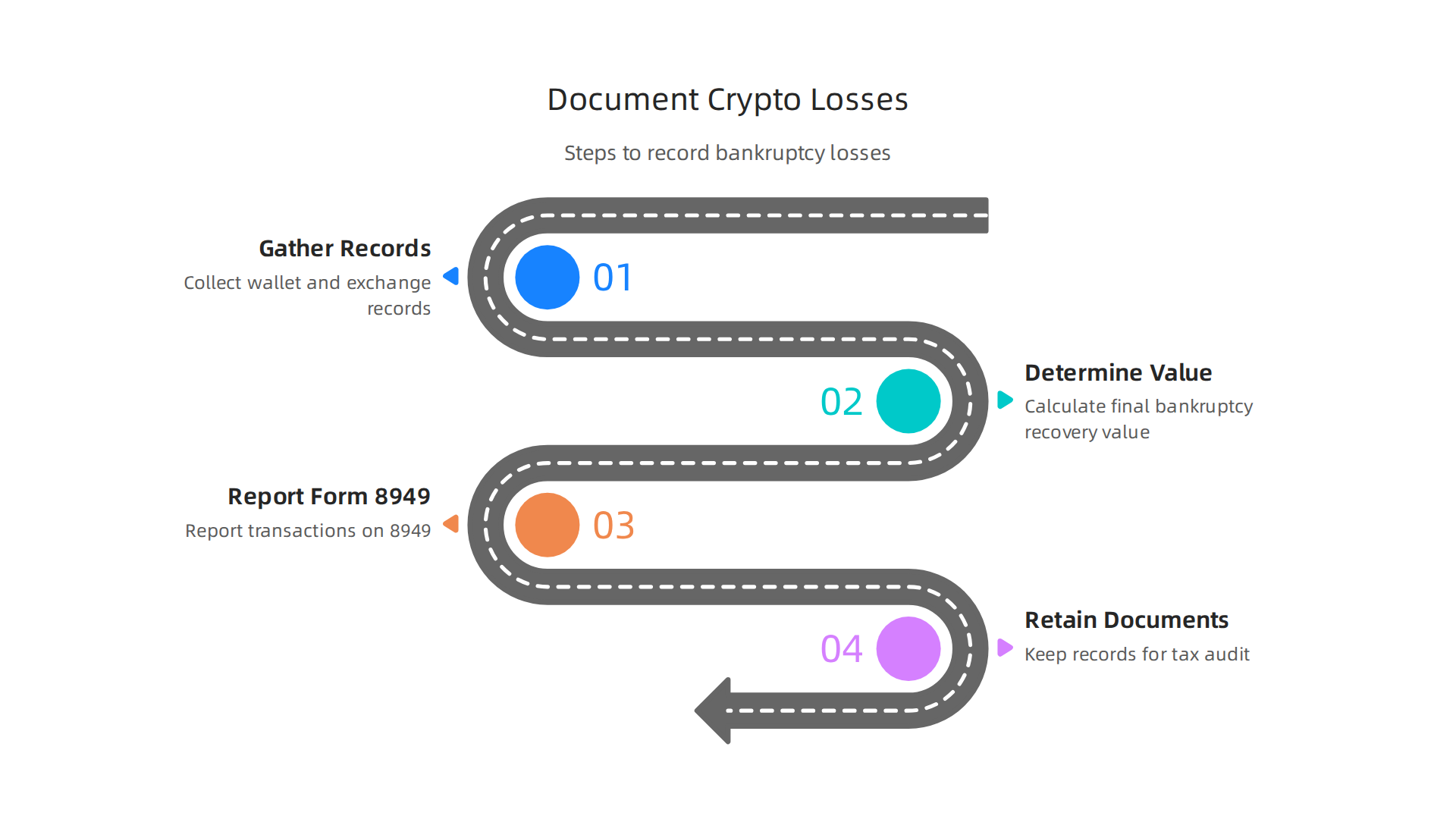

Step-by-step guidance for documenting bankruptcy losses

Follow these steps to stay safe in 2026.

Step 1: Gather your records. Pull all transaction histories from the failed exchange. Note the date it froze withdrawals and the value of your coins on that date. The White House recommended clearer rules for digital asset transactions, and the IRS has updated its guidance this year.

Step 2: Determine the final value. Once the bankruptcy plan is approved, find out what you actually recovered. Subtract that from your original cost basis. That is your loss.

Step 3: Report using Form 8949. List each coin or token separately. Attach a statement explaining the bankruptcy. The new Form 1099-DA will also show your recovery amount if your broker issued one.

Step 4: Keep all documents. The IRS can audit up to six years later. Save court filings, plan summaries, and correspondence.

What if you still owe taxes from past years?

Many investors got confused and didn’t file losses when they should have. If you owe back taxes because of this, the IRS offers an offer in compromise program. This lets you settle for less than the full amount.

But the best approach is to get ahead of the confusion. For clear, weekly updates on bankruptcy tax rules and other crypto changes, subscribe to the free Clicks and Trades newsletter. You will get plain English guidance sent right to your inbox. Sign up here.

Staying Compliant: Practical Steps for Crypto Taxpayers in 2026

You now understand how bankruptcies and lawsuits create tax trouble. But the real challenge is staying on top of your filings before problems start. In 2026, the IRS has more tools than ever to find mistakes. The good news? A few simple habits can keep you safe.

Good recordkeeping is your best defense

Accurate records are the backbone of compliant crypto taxes. Without them, you cannot prove your cost basis or show the IRS what happened during a bankruptcy or lawsuit.

The simplest method is using a dedicated crypto tax platform. These tools connect to your exchanges and wallets, pull transaction histories, and calculate your gains automatically. The CoinLedger guide to crypto taxes explains how these platforms work and why they save hours of manual work.

If you prefer spreadsheets, at minimum track these details for every trade:

- Date and time of transaction

- Type of crypto bought or sold

- Amount and fair market value in USD

- Purpose of the transaction (trade, spend, gift, etc.)

Save all exchange and wallet export files in a dedicated folder. Keep them for at least seven years. The IRS can audit returns up to six years back, especially if they suspect underreporting.

Common audit red flags in 2026

Thanks to the new Form 1099-DA, brokers now report your crypto activity directly to the IRS. This means mismatches between what you report and what the IRS receives are easier to spot.

According to the CountDeFi blog, common triggers include:

- High transaction volume with no reported gains or losses

- Staking or lending rewards that you did not report as income

- Large transfers between wallets that are not documented

- Using different cost basis methods inconsistently

The HackerJohnson article on audit triggers notes that taxpayers earning over $400,000 face higher audit rates in 2026. But even smaller investors can get flagged if their records do not match.

The White House has also weighed in. Their recommendations on digital asset transactions were included in the IRS Priority Guidance Plan. This means clearer rules are coming, but also stricter enforcement.

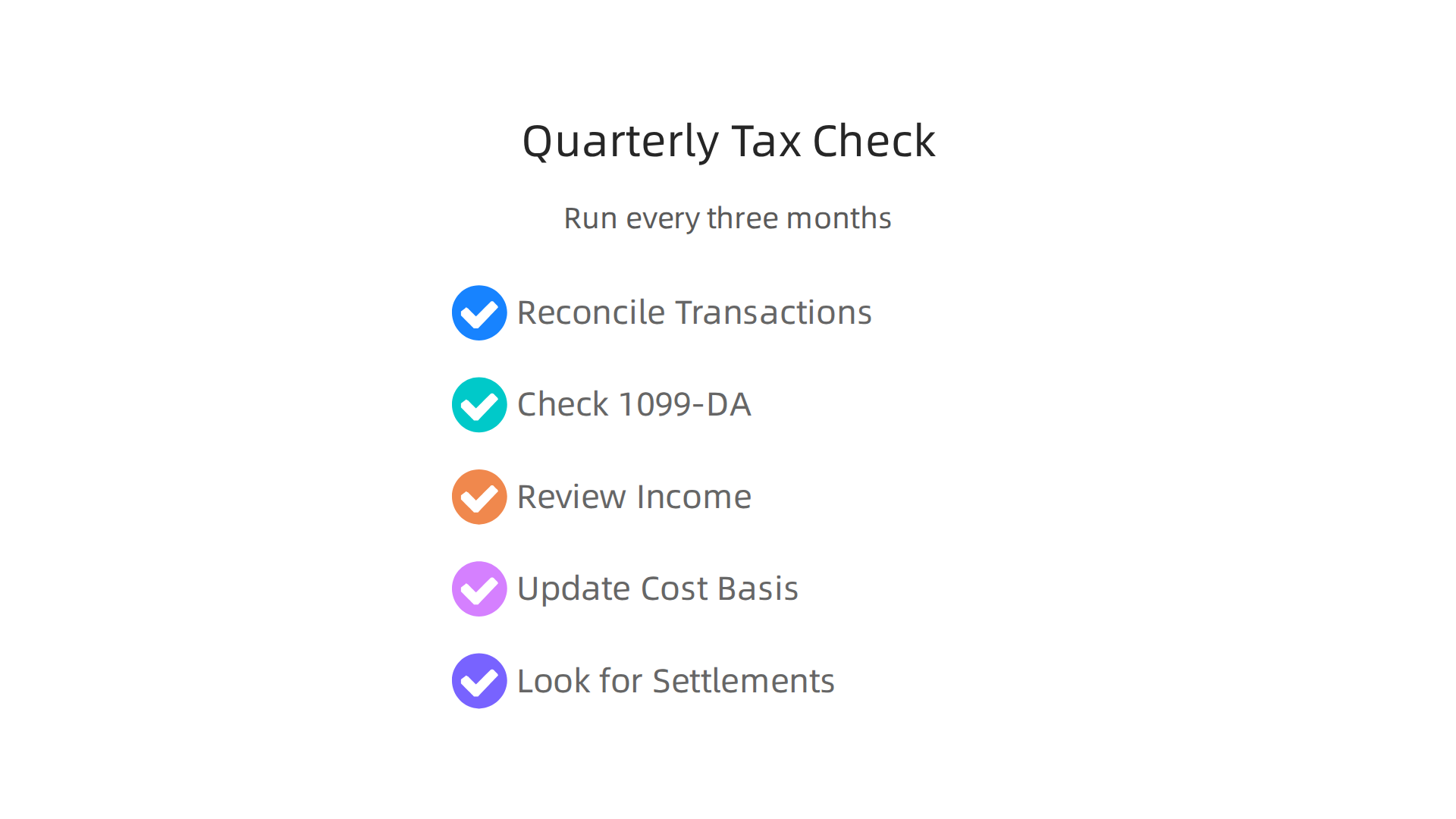

Quarterly tax health check checklist

Set a reminder every three months to run through this short list.

It takes 15 minutes and saves you stress in April.

- Reconcile your transactions. Compare your records with exchange statements and wallet histories. Fix any missing or duplicate entries.

- Check for new 1099-DA forms. Make sure your brokers have issued them. If not, follow up.

- Review staking and DeFi income. Any rewards you earned are taxable as ordinary income. Report them accurately.

- Update your cost basis method. The IRS extended relief on reporting methods through 2026. You can still use FIFO or specific identification. Pick one and stay consistent.

- Look for bankruptcy or lawsuit settlements. If you received a partial refund, note the date and value. This will affect your capital gains calculations.

For deeper guidance on setting up your own bookkeeping system, read our post on crypto taxes: the 2026 guide to avoiding penalties and audits. It walks you through the exact steps to build audit-proof records.

Stay ahead with weekly updates

The rules keep changing. Bankruptcy cases settle, new forms appear, and the IRS updates its focus areas. You do not need to track all of this alone.

The free Clicks and Trades newsletter delivers plain English updates on crypto taxes, bankruptcy fallout, and compliance tips right to your inbox. Sign up here and get a weekly checklist to keep your crypto tax stress low.

Looking Ahead: Crypto Tax Trends and How to Prepare for 2027

You have mastered 2026 compliance. Smart. But the tax landscape is shifting fast. The real question is: what comes next?

How White House Policy Is Reshaping Crypto Taxes

The current administration is pushing hard to make the US the “crypto capital of the world.” The White House signed an executive order to support the responsible growth of digital assets. It also established a Strategic Bitcoin Reserve and the US Digital Asset Stockpile.

These moves sound positive. But they also invite stricter rules. The White House has hosted meetings with crypto leaders and the Treasury to discuss market structure and the GENIUS Act. One official even predicted a crypto boom after legislation passes. More activity means more taxable events.

What Lawsuits and Bankruptcies Mean for 2027

You already know how cryptocurrency bankruptcies and crypto lawsuits create tax headaches. In 2027, expect that trend to continue. Settlements and partial refunds will still need careful tracking. The White House report on crypto tax changes recommends adding digital assets to the list of assets subject to wash sale rules. If passed, tax loss harvesting on crypto could end.

Predictions for Staking, DeFi, and NFT Taxes

The IRS is actively watching DeFi and staking. While no specific DeFi tax law exists yet, the Koinly guide on DeFi taxes reminds us that existing property rules apply to every swap and yield farm. Staking rewards are taxable as ordinary income when received, and long term holdings get capital gains treatment if held over a year, as outlined in the staking taxes guide from CoinTracking.

Experts expect clearer rules for NFTs and DeFi by late 2026 or early 2027. The 2026 crypto tax forecast from Cadwalader notes that legislation like the CLARITY Act could define what counts as a digital asset and how it is taxed.

How to Prepare Now

You do not need a crystal ball. You need a system.

First, set up audit ready records today. Use a dedicated crypto tax tool to track every trade, stake, and airdrop. Second, stay informed. Rules change fast, and the best way to avoid surprises is to know what is coming.

The free Clicks and Trades newsletter sends weekly updates on white house crypto policy, cryptocurrency bankruptcy fallout, and new IRS guidance. It helps you spot trends before they turn into tax problems. Sign Up and get the clarity you need to navigate 2027 with confidence.

Summary

This article explains how White House crypto policy and 2026 IRS guidance directly change what crypto investors must report and pay. It covers the most important practical rules: staking rewards are taxable when received, most DeFi interactions are now treated as taxable events, and settlements or recoveries from lawsuits and bankruptcies can create unexpected capital gains. The piece shows how to claim worthlessness or bankruptcy losses, how to report recoveries on Form 8949 (and reconcile new 1099-DA forms), and when legal fees may or may not be deductible. It also gives a clear recordkeeping system, a quarterly checklist to avoid audits, and steps to document losses and refunds. Readers will learn concrete actions—what to save, how to calculate gains or losses, and which forms to use—so they can file accurately and reduce audit risk. The article emphasizes simple habits and tools to stay compliant as rules evolve into 2027.

By

April 28, 2026