Unlock Easy Crypto Taxes with a Federal Tax Calculator 2026

Why a Federal Tax Calculator Can Save You Time and Reduce Surprises

Do you ever feel a little lost when it comes to your crypto taxes? It’s a common feeling.

Many people find themselves confused by all the different rules. They might not know what counts as a taxable event or how to keep good records. This can lead to big, unexpected tax bills or worries about making mistakes with the IRS. Actually, the IRS treats virtual currency, like Bitcoin, as property. This means things like selling, trading, or even spending your crypto can create a taxable event for federal income tax purposes, according to the IRS guidelines updated for 2026, and requires reporting on your tax return 2026, as noted by the IRS itself.

This is where a good federal tax calculator for crypto comes in handy. It’s more than just a tool to estimate how much you owe. A specialized crypto federal tax calculator helps you understand the complex world of digital assets and their tax rules. It helps you keep track of all your transactions, which is super important because you need to report all digital asset transactions accurately.

You see, whether you’re selling crypto, getting paid in it, or doing other digital asset transactions, you need to report it on your tax return. A reliable calculator can help you figure out your capital gains or losses, and even income from things like staking or mining, which might affect your self employment tax if you’re working for yourself. If you’re wondering how to calculate tax on your crypto, this guide will give you clear steps.

In this guide, we’ll walk you through how a federal tax calculator works. We’ll give you a simple checklist for keeping good records and show you how to estimate your tax liability safely, so there are no big surprises. Getting organized now can save you a lot of stress later, and it helps you stay compliant with tax laws in 2026. For more simple guides and tips, you can also check out the free newsletter from Clicks and Trades. It’s a great way to get more step-by-step crypto education and safety advice.

Ready to take control of your crypto tax journey?

A federal tax calculator for crypto is like having a special assistant for your digital money. It does more than just show you a number.

It helps you sort through all your crypto actions so you can report them correctly to the IRS in 2026. Think of it as a bridge between your crypto activities and your tax return.

Core Functions of a Crypto Federal Tax Calculator

So, what exactly does this helpful tool do?

- Imports Your Transactions: First, it brings in all your crypto trades and activities. This means connecting to your exchanges, wallets, and even some DeFi apps. It pulls in data about when you bought, sold, traded, or moved your crypto. Many of these calculators can easily import from various sources, making it simple to gather all your records in one place, which is a key feature of the best crypto tax software available in 2026, according to expert reviews (NerdWallet, Bitbo, CoinSutra).

- Finds Taxable Events: Next, it looks at all that data to figure out what counts as a "taxable event." This could be selling Bitcoin for cash, trading Ethereum for Solana, or even using crypto to buy something. The calculator helps you see which actions mean you might owe tax.

- Figures Out Gains and Losses: This is a big one. When you sell crypto, the calculator helps you how to calculate tax on your profit or loss. It takes what you paid for the crypto (your "cost basis") and compares it to what you sold it for. If you sold for more, that’s a capital gain. If you sold for less, that’s a capital loss.

- Sorts Income vs. Capital Events: Not all crypto activity is about buying and selling. If you earn crypto through staking, mining, or getting airdrops, that’s usually seen as income. A good federal tax calculator helps separate these income events from capital gains and losses. This is important because income might be taxed differently, and could even affect your self employment tax if you’re a miner or staker working for yourself.

How Calculators Handle Your Crypto’s Cost

One of the trickiest parts of crypto taxes is figuring out your "cost basis." This is simply how much you paid for your crypto, plus any fees. The calculator uses different ways to match up what you bought with what you sold:

- FIFO (First-In, First-Out): This is like pulling items from a stack. The first crypto you bought is the first one you’re considered to sell. This is a common method.

- Specific Identification: Sometimes, you can choose exactly which piece of crypto you’re selling. For example, if you bought Bitcoin at different prices, you might want to sell the one that results in the smallest gain or a loss to lower your tax bill. A good calculator can help you track these specific amounts.

- Special Events: What about when a new coin is created from an old one (a hard fork) or you get free crypto (an airdrop)? A good calculator tries to handle these tricky situations, though you might still need to understand the rules.

Keeping good records throughout the year is key to helping any calculator work best. For more tips on staying organized, check out our guide on how to avoid tax chaos and stress with crypto bookkeeping.

Important Things to Remember

Even with a smart federal tax calculator, there are a few things to keep in mind:

- Rules Differ by Location: While we’re talking about federal taxes in the U.S., tax rules for crypto can be different in other countries. More than sixty countries are working on ways to deal with crypto tax risks and regulation in 2026 (PwC Global Crypto Tax Report 2026, OECD). Some places, like France, even have a flat rate for crypto gains, as discussed in recent reports on cryptocurrency taxation (Cryptocurrency Taxation: Regulatory Challenges and Legal).

- Complex Crypto Can Be Tricky: If you do very complex things with DeFi (Decentralized Finance) or many unique NFT trades, the calculator might still need your help to sort everything out. These areas are quickly changing and can be tough even for advanced tools.

- Manual Check is Smart: Always review what the calculator gives you. It’s a great tool, but it’s always good to understand how it reached its numbers. This helps you catch any mistakes before you file.

In short, a federal tax calculator for crypto is a powerful tool to help you understand your crypto gains, losses, and income.

It helps you stay organized and feel more confident about your taxes.

Ready to simplify your crypto tax journey?

One of the trickiest parts of crypto taxes is figuring out your "cost basis." This is simply how much you paid for your crypto, plus any fees. The calculator uses different ways to match up what you bought with what you sold. Let’s look at the main methods a federal tax calculator uses to help you how to calculate tax on your crypto profits.

FIFO (First-In, First-Out)

Imagine you buy a bunch of apples and stack them up. When you take an apple to eat, you usually grab the one you bought first, right? That’s how FIFO works for crypto. It means the first cryptocurrency you bought is considered the first one you sell when you make a trade. The IRS often sees FIFO as the default method for crypto if you don’t choose another one [^1, ^7]. A federal tax calculator will use this method to automatically figure out your gains and losses unless you tell it otherwise.

Specific Identification (Specific ID)

With Specific ID, you get to choose exactly which piece of crypto you’re selling from your holdings [^2]. Let’s say you bought Bitcoin at different prices throughout the year. If you sell some Bitcoin, you might want to pick the "lot" (a specific purchase) that helps you pay less tax. For example, you might pick a lot you bought for a higher price to show a smaller profit, or even a loss, to lower your tax bill. The IRS supports Specific ID, but you need good records to prove which specific crypto you sold [^6].

Why Your Choice Matters

The method you choose can really change your tax bill. Using FIFO might lead to a higher profit (and thus more tax) if the price of your crypto has generally gone up over time. But with Specific ID, a good federal tax calculator can help you pick the best "lots" to sell. This can help you reduce your capital gains or increase your capital losses, which can save you money on taxes. Many calculators let you switch between these methods to see which one works best for you and your yearly tax estimates [^4].

Common Problems

To use Specific ID well, your crypto wallet or exchange needs to provide very clear records. If the data is messy or incomplete, the calculator might not be able to match up your specific buys and sells properly. This can make it hard to get the tax benefits of Specific ID. That’s why keeping good records all year is super important [^3]. For more tips on keeping your crypto records in order, check out our guide on how to avoid tax chaos and stress with crypto bookkeeping.

A federal tax calculator acts like your smart assistant. It helps you sort through these important cost methods to figure out your crypto taxes correctly. For more step-by-step crypto education, safety tips, and clear guidance, consider subscribing to the free Clicks and Trades newsletter.

Ready to simplify your crypto tax journey?

After understanding how a federal tax calculator figures out your cost basis, the next big step is knowing when you actually owe tax. It’s not just about selling crypto for cash. Many different things you do with crypto can be "taxable events." This means the IRS sees it as a moment when you either made money (a gain) or lost money (a loss), and you need to report it.

The most important thing to know is that the IRS treats virtual currency, like Bitcoin or Ethereum, as "property." This is similar to how they treat stocks or other investments, not like regular money [^1, ^9]. Because it’s property, any time you get rid of it, it’s usually a taxable event.

Here are the most common things that count as taxable events and trigger capital gains or losses:

- Selling Crypto for Cash: If you sell Bitcoin for U.S. dollars, that’s a taxable event. If you sold it for more than you paid, you have a capital gain. If you sold it for less, you have a capital loss [^3, ^8].

- Trading One Crypto for Another: This is a big one many people miss! If you trade Bitcoin for Ethereum, or any crypto for another, the IRS sees this as first selling your Bitcoin and then using the proceeds to buy Ethereum. Both steps count as a taxable event [^4, ^15].

- Using Crypto to Buy Things: Let’s say you use Bitcoin to pay for a coffee or a new computer. That’s also a taxable event. The IRS views it as you selling the Bitcoin to get the item [^3, ^8].

It’s important to remember that simply moving your crypto from one wallet you own to another wallet you own is generally not a taxable event [^2, ^13]. It’s just like moving cash from your checking account to your savings account.

Crypto Activities That Create Ordinary Income

While sales and trades create capital gains or losses, some crypto activities are more like earning a paycheck. These are taxed as "ordinary income," which usually means your regular income tax rate applies, just like your salary or wages. A federal tax calculator can help you keep these types of income separate.

Here are some common examples:

- Mining Crypto: If you mine new cryptocurrency, the value of that crypto at the moment you receive it is considered ordinary income [^11, ^12].

- Staking Rewards: When you "stake" your crypto and earn rewards, those rewards are taxed as ordinary income when you get them [^4, ^11].

- Airdrops: If you receive free crypto through an airdrop, the fair market value of that crypto on the day you receive it is considered ordinary income [^12, ^13].

Special Considerations for DeFi Activity

Decentralized Finance, or DeFi, adds another layer of complexity. With DeFi, you might be interacting with special apps on the blockchain to lend, borrow, or swap tokens without a middleman. These actions can create many taxable events.

For example:

- Token Swaps: Just like trading on a regular exchange, swapping tokens on a decentralized exchange (DEX) is a taxable event. You’re disposing of one token to get another [^10].

- Providing Liquidity: When you put your crypto into a liquidity pool, you usually get special "LP tokens" in return. Adding or removing your crypto from these pools, or even receiving rewards from them, can all trigger taxable events. The rules for these are still developing, but it’s best to track everything [^10].

Because these activities can create a lot of individual transactions, using a federal tax calculator is super helpful. It connects to your wallets and exchanges, pulls in all your activity, and helps you how to calculate tax for each step. This way, you don’t miss anything the IRS cares about [^6].

Keeping a close eye on all these different types of events throughout the year is key to avoiding surprises. If you want more help tracking these complex transactions and making sure you avoid any issues, learning how to properly report everything is vital. Check out our guide on Crypto Taxes: The 2026 Guide to Avoiding Penalties and Audits.

For ongoing education and clear guidance on your crypto tax journey, remember to subscribe to the free Clicks and Trades newsletter.

Ready to simplify your crypto tax journey?

Having a good grasp of what counts as a taxable event is super important. Now, let’s talk about how a federal tax calculator can make figuring out your crypto taxes much simpler. These handy tools are like your personal assistant for crypto taxes, helping you how to calculate tax on all your different activities [^1]. They can help you estimate what you owe for federal taxes right here in 2026.

Here’s a step-by-step look at how you might use one.

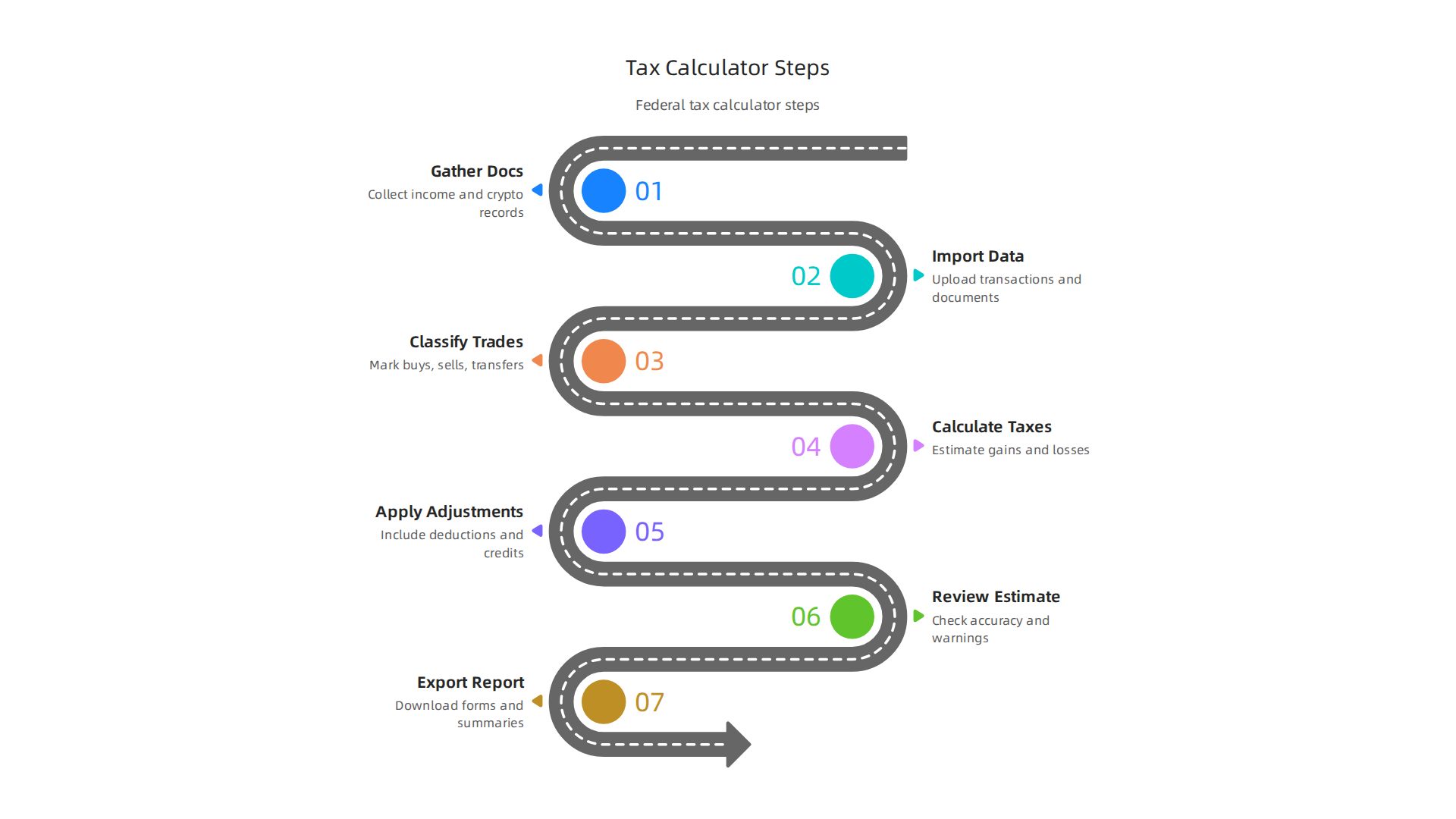

Getting Ready: Your Pre-Checks

Before you jump into a federal tax calculator, you need to do a little prep work. Think of it like getting all your ingredients ready before you start cooking.

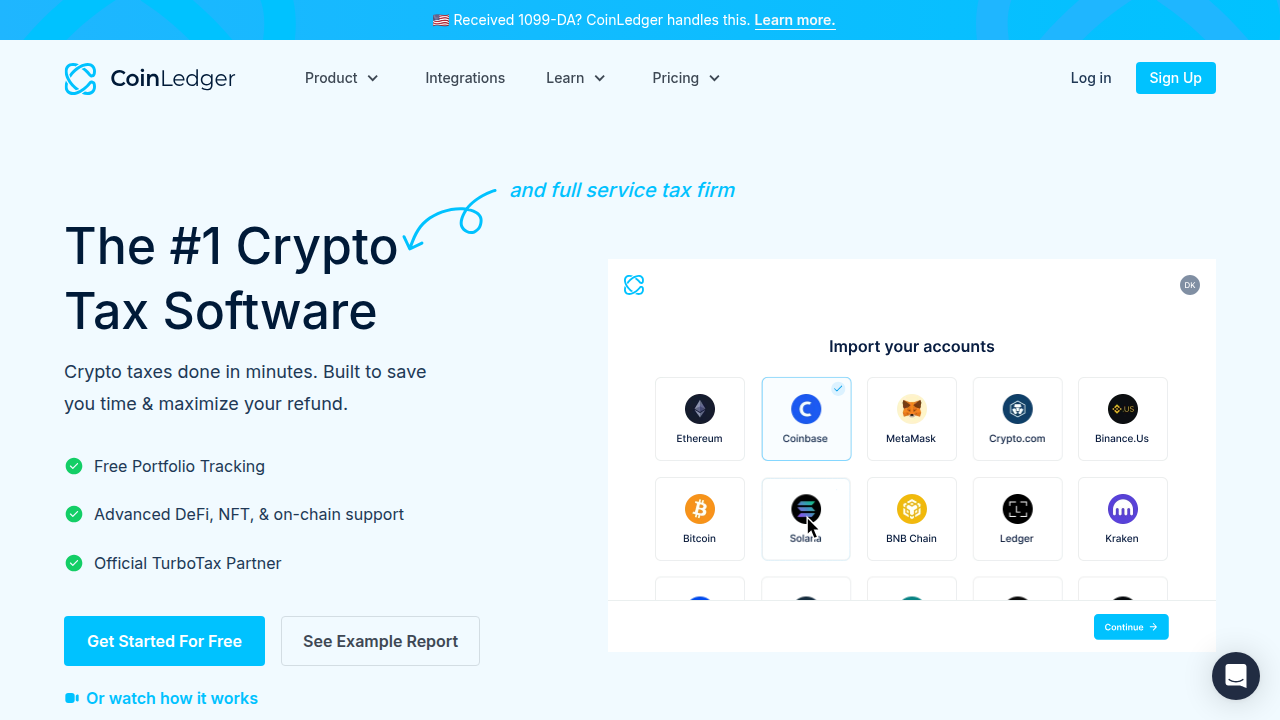

- Gather Your Accounts: Write down every exchange, wallet, and DeFi platform you’ve used. This includes big names like Coinbase or Binance, your Ledger wallet, and any decentralized apps where you did swaps or staking. The more complete your list, the better.

- Export Your Data: Most crypto tax software will let you link your accounts directly (using API keys) or upload files. If you can’t link, you’ll need to download your transaction history from each platform. Look for a "transaction history" or "export CSV" option. This file lists every buy, sell, trade, and transfer you made [^4].

- Pick Your Cost-Basis Method: This is how you tell the calculator how to figure out your profit or loss. The most common methods are FIFO (First-In, First-Out) and LIFO (Last-In, First-Out). FIFO usually means you sell the crypto you bought earliest first. LIFO means you sell the crypto you bought most recently first. Your choice can impact your tax bill, so it’s a good idea to understand which one works best for you.

Using the Calculator: Your Step-by-Step Walkthrough

Now that your data is ready, let’s put that federal tax calculator to work.

- Import Your Transactions: Open your chosen crypto tax software. Many popular tools like CoinLedger, Koinly, or TokenTax make this easy

[^2, ^5, ^3]. You’ll connect your exchanges and wallets, or upload those CSV files you prepared. The software will pull in all your crypto moves.

2. Map Wallets and Exchanges: The calculator will try its best to understand your transactions. Sometimes it needs a little help. For example, if you sent Bitcoin from your Coinbase account to your Ledger wallet, the software might see it as a "withdrawal" from Coinbase and a "deposit" to Ledger. You might need to tell it, "Hey, this was just a transfer between my own wallets, not a sale!" This helps it avoid counting a non-taxable event as taxable.

3. Verify Transactions: Look through the list of transactions the calculator shows you. Does everything seem right? Did it correctly identify a trade of Bitcoin for Ethereum as a taxable event, or a gift of crypto from a friend? Taking your time here makes sure your tax report is accurate.

4. Classify Income vs. Capital Events: Remember from before that some crypto activities create ordinary income (like mining or staking rewards), while others create capital gains or losses (like selling or trading). A good federal tax calculator will usually try to sort these for you. You may need to review and confirm these classifications, especially for complex DeFi actions or airdrops [^6].

5. Run the Estimate: Once all your transactions are in and correctly classified, the federal tax calculator can crunch the numbers. It will calculate your capital gains and losses, your ordinary crypto income, and give you an estimate of your overall tax liability. Some even help you figure out how to calculate sales tax if you used crypto to buy goods in certain states, or even your self employment tax if you’re a miner or validator.

After the Run: Reviewing and Getting Ready to File

You’re almost there! Don’t just close the program after seeing the estimate.

- Review Flagged Items: Most calculators will flag transactions they’re unsure about. These might be missing cost basis details, unclear transfers, or tricky DeFi moves. Go through these flagged items and fix them. This is crucial for an accurate tax report.

- Reconcile with Your Records: Compare the calculator’s summary with your own notes or spreadsheets. Does the total number of transactions seem right? Are the overall gains and losses what you expected? If something looks way off, investigate it.

- Export Reports: Once you’re happy with the results, you can export various reports. These often include IRS Form 8949, income reports, and full transaction histories. These reports are what you’ll use to file your taxes or give to a tax professional [^8]. Many popular tax software, like TurboTax, also allow direct import from these crypto tax tools, making filing even smoother [^7].

Using a federal tax calculator really takes the guesswork out of crypto taxes in 2026. It helps you stay organized and confident.

Ready to simplify your crypto tax journey?

Sign Up

Now that your crypto transaction data is ready, the next big step with your federal tax calculator is getting it all into the software. This is where you connect your accounts or upload files. It sounds simple, but sometimes you need to do a little detective work to make sure everything is just right.

Importing transaction histories: CSVs, APIs, and manual corrections

Bringing all your crypto history into a federal tax calculator is often the first real step to figure out how to calculate tax. Most good calculators offer two main ways to do this: connecting through an API or uploading CSV files.

- API connections are like a direct link between your exchange (like Coinbase or Binance) and the tax software. You give the software permission to read your transaction history straight from the exchange. This is often the easiest and fastest way to get your data in. Many popular tools like CoinLedger, Koinly, or TokenTax work this way, making crypto tax reporting straightforward [^2, ^3, ^5].

- CSV (Comma Separated Values) files are basically spreadsheets of your transactions. You download these files from your exchanges, wallets, or DeFi platforms, then upload them to your

federal tax calculator. This is handy for platforms that don’t offer direct API connections, or if you prefer to have a copy of your data yourself. Keep in mind that different platforms might format their CSVs a little differently, which can sometimes lead to small hiccups.

Spotting and fixing mismatches

Even with good import methods, crypto transactions can be tricky. You might find:

- Duplicate transactions: Sometimes, if you import from two different places, the same transfer might show up twice. For example, a transfer from Exchange A to Wallet B might be recorded as a "withdrawal" from A and a "deposit" to B. You’ll need to tell your

federal tax calculatorthat these are two sides of the same coin, not two separate events. - Missing cost-basis: This is crucial. Your "cost-basis" is what you originally paid for your crypto. If the calculator doesn’t know this, it can’t figure out your profit or loss when you sell or trade [^9]. This often happens with older crypto holdings, transfers from wallets not fully linked, or complex DeFi moves. The IRS generally expects you to use methods like FIFO (First-In, First-Out) for tracking your cost basis [^15]. If your software shows "missing cost-basis" for some transactions, you’ll need to find that original purchase data and add it in.

- Chain-swap anomalies: When you move crypto from one blockchain to another, like changing Wrapped Bitcoin (WBTC) on Ethereum to Bitcoin on the native network, the tax software might sometimes see this as a sell and a buy, rather than a transfer. Review these carefully.

When manual fixes are necessary

Because crypto is still quite new and always changing, automatic imports aren’t always perfect. Sometimes you’ll need to do some manual work:

- Tagging transactions: You might need to tell your

federal tax calculatorif a transaction was a gift, a donation, income from staking or mining, or just a transfer between your own wallets. This helps the calculator sort income from capital gains, which is important for your overall tax picture [^6]. - Exchange-specific mapping: Some DeFi or smaller exchanges might have unique ways of logging transactions. The calculator might need you to "map" or categorize these transactions so it understands what they mean.

Taking the time to review and correct these details ensures your crypto tax report is accurate. It really makes a difference when it’s time to file, helping you avoid surprises and ensuring you correctly figure out how to calculate tax. For more help with keeping good records, check out our guide on how to avoid tax chaos and stress with proper bookkeeping: The 2026 Crypto Bookkeeping Guide: Avoid Tax Chaos and Stress.

Using a federal tax calculator can be a huge time-saver, but it still needs your careful eye to make sure the data is clean. This attention to detail will help you prepare for filing your taxes with confidence.

Ready to simplify your crypto tax journey? Sign Up

When you dive deeper into crypto, you find special activities like staking, mining, airdrops, NFTs, and DeFi. Each of these has its own set of rules for taxes. A good federal tax calculator helps you sort through these, but it’s helpful to know the basics of how they’re treated. This knowledge will guide you on how to calculate tax for these unique situations in 2026.

How Calculators Treat Staking and Mining

Let’s start with staking and mining. These are ways people can earn new crypto.

- Staking is like earning interest by holding your crypto in a special wallet to help a blockchain network run smoothly.

- Mining is when you use powerful computers to solve puzzles and verify transactions, earning new crypto as a reward.

For tax purposes, the crypto you get from staking rewards or mining is usually seen as ordinary income. This means it’s taxed just like the money you earn from a job or interest from a bank account [^2, ^3]. You typically owe tax on these rewards at the moment you receive them, based on their fair market value at that time [^4].

Your federal tax calculator will usually add these rewards to your income. The value of the crypto when you received it then becomes its "cost basis." This cost basis is super important because if you later sell that staked or mined crypto, your profit or loss is figured out using this original value [^6]. If you’re a self-employed miner or staker, this income might also be subject to self-employment tax.

Airdrops and Forks

- Airdrops are like free giveaways of crypto. A new project might send tokens to many wallets to get the word out.

- Hard forks happen when a blockchain splits, creating a new cryptocurrency from an existing one you hold.

Just like staking and mining, crypto received from airdrops and hard forks is typically taxed as ordinary income when you get it [^2, ^3]. Your federal tax calculator should record the value of these assets on the day you received them as income. That value also becomes their cost basis. If you decide to sell them later, any profit or loss will be a capital gain or loss.

NFTs and DeFi: Royalties, Loans, and Liquidity Mining

NFTs and DeFi are some of the newer, more complex areas in crypto. The IRS still has not released specific guidance for all DeFi activities, so rules can be tricky [^1]. However, a good federal tax calculator can help you manage these.

- NFTs (Non-Fungible Tokens): These are unique digital items. When you buy and sell NFTs, it’s generally treated like buying and selling other property. This means you’ll have a capital gain if you sell for more than you paid, or a capital loss if you sell for less [^7, ^8]. If you create an NFT and earn royalties each time it’s resold, those royalties are seen as ordinary income. Your federal tax calculator tracks these sales and income events.

- DeFi (Decentralized Finance): This covers a wide range of services on the blockchain, like lending, borrowing, and providing liquidity.

- Lending and Borrowing: If you lend out your crypto and earn interest, that interest is typically seen as ordinary income. Using crypto as collateral for a loan is usually not a taxable event unless you lose the collateral due to not repaying the loan.

- Liquidity Mining and Yield Farming: When you provide crypto to a pool to help trades happen and earn rewards for it, those rewards are generally considered ordinary income when you receive them.

A federal tax calculator will try its best to correctly categorize all these different transactions. But because DeFi is still so new and complex, you might need to step in and tag some transactions yourself to make sure they are reported correctly.

Understanding these special activities is a big part of knowing how to calculate tax for all your crypto dealings. While a federal tax calculator does a lot of heavy lifting, your careful review ensures everything is accurate. For more help navigating these complexities and avoiding common tax pitfalls, you might find our guide on Crypto Taxes: The 2026 Guide to Avoiding Penalties and Audits very useful.

Remember, staying informed is key. For ongoing step-by-step crypto education, safety tips, and clear guidance, consider exploring resources like the free Clicks and Trades newsletter. It’s a great way to keep up with the changing world of crypto and taxes.

Ready to gain more confidence in managing your crypto tax obligations?

Sign Up for helpful insights.## How Calculators Treat Staking, Mining, Airdrops, NFTs, and DeFi (Special Activities)

As you get more involved with crypto, you might encounter special activities like staking, mining, airdrops, NFTs, and DeFi. Each of these has specific tax rules. A good federal tax calculator can help you understand these rules and how to calculate tax for each activity. In 2026, it’s more important than ever to get these details right.

Staking and Mining Rewards

Staking and mining are ways people earn new crypto.

- Staking means you hold your crypto in a special wallet to help a blockchain network run smoothly. For doing this, you earn rewards.

- Mining involves using strong computers to solve puzzles and confirm transactions, earning new crypto as payment.

The crypto you get from staking or mining is usually seen as ordinary income. This means it is taxed like money you earn from a job or interest from a savings account [^2, ^3]. You typically owe tax on these rewards when you receive them, based on their value at that time [^4].

Your federal tax calculator will add these rewards to your income. The value of the crypto when you received it then becomes its "cost basis." This cost basis is very important because if you later sell that crypto, your profit or loss is figured out using this starting value [^6]. If you earn a lot from mining or staking, you might also need to consider self-employment tax.

Airdrops and Forks Explained

- Airdrops are like free giveaways of crypto. A new project might send tokens to many wallets to spread the word.

- Hard forks happen when a blockchain splits into two, creating a new cryptocurrency from one you already own.

Similar to staking and mining, crypto you get from airdrops and hard forks is typically taxed as ordinary income when you receive it [^2, ^3]. Your federal tax calculator should record the value of these assets on the day you got them as income. That same value also becomes their cost basis. If you sell them later, any profit or loss will be a capital gain or loss.

NFTs and DeFi: What Your Calculator Needs to Know

NFTs and DeFi are some of the newer and more complex parts of the crypto world. The IRS has not given specific guidance for all DeFi activities yet, making some tax rules tricky [^1]. Still, a good federal tax calculator can help you manage these situations.

- NFTs (Non-Fungible Tokens): These are unique digital items. When you buy and sell NFTs, it is generally treated like buying and selling other property. This means you’ll have a capital gain if you sell an NFT for more than you paid, or a capital loss if you sell it for less [^7, ^8]. If you create an NFT and earn royalties each time it’s resold, those royalties are considered ordinary income. Your federal tax calculator tracks these sales and income events.

- DeFi (Decentralized Finance): This covers many financial services on the blockchain, such as lending, borrowing, and providing liquidity.

- Lending and Borrowing: If you lend your crypto and earn interest, that interest is typically seen as ordinary income. Using crypto as collateral for a loan is usually not a taxable event unless you lose the collateral because you did not repay the loan.

- Liquidity Mining and Yield Farming: When you provide crypto to a pool to help trades happen and earn rewards for it, those rewards are usually considered ordinary income when you receive them.

A federal tax calculator will do its best to correctly sort all these different transactions. But because DeFi is still so new and quickly changing, you might need to manually tag some transactions to ensure they are reported correctly.

Understanding these special activities is a big part of knowing how to calculate tax for all your crypto dealings. While a federal tax calculator does much of the hard work, your careful check makes sure everything is accurate. For more help navigating these complex areas and avoiding common tax problems, you might find our guide on Crypto Taxes: The 2026 Guide to Avoiding Penalties and Audits very helpful.

Staying informed is important. For ongoing, easy-to-understand crypto education, safety tips, and clear guidance, consider checking out the free Clicks and Trades newsletter. It’s a great way to stay updated with the fast-moving world of crypto and taxes.

Ready to feel more confident managing your crypto tax responsibilities?

Sign Up for helpful insights.

After learning how different crypto activities like staking, mining, airdrops, NFTs, and DeFi are taxed, the next important step is keeping good records. Having a solid file of documents is key to avoiding problems with tax authorities, like an audit. Even the best federal tax calculator can only do so much if it doesn’t have good information to start with. In 2026, with more eyes on crypto activities, building an "audit-ready" file is super important [^1, ^2].

Essential Documents for Your Crypto File

Think of your crypto records as proof of everything you’ve done. These documents help show exactly when you bought or sold crypto, for how much, and where it went.

Here are the main things you should keep:

- Transaction Exports: These are reports you can get from your crypto exchanges and wallets. They show all your buys, sells, trades, and transfers.

- Wallet Address Logs: Keep a record of all the different crypto wallet addresses you use. This helps connect transactions to you.

- Receipts for Purchases or Sales: If you used regular money (like dollars) to buy crypto or NFTs, or if you sold them for regular money, keep those receipts.

- Trade Pair Mapping: This simply means keeping track of what crypto you traded for another crypto. For example, if you traded Bitcoin for Ethereum.

These details help your federal tax calculator figure out your cost basis and any gains or losses.

How to Keep Your Records Organized

Keeping your files neat makes tax time much easier, and it helps if someone from the tax office ever has questions. Tax authorities worldwide are focusing more on crypto, so good records are a must [^4].

- Keep Records for Many Years: It’s smart to hold onto your tax documents, including crypto records, for at least three to seven years.

- Go Digital: Storing your documents digitally is often easiest. You can create folders on your computer or in cloud storage.

- Structure Your Files: Organize your files by year first. Inside each year’s folder, you can make sub-folders for each exchange or wallet you used. This way, if you need to find something, it’s quick and easy.

Proper organization also helps when you need to use different ways to calculate your crypto cost basis, like First-In, First-Out (FIFO) or Specific Identification. These methods affect how your profits or losses are figured out [^10, ^12]. The IRS even extended temporary relief for choosing crypto lots through 2026, so knowing your options and having clear records is key [^17].

Using Your Federal Tax Calculator for Audit Reports

Many federal tax calculators can create special reports, sometimes called "audit reports" or "worksheets." These reports summarize your crypto activity, including income, capital gains, and losses. They can be a big help in showing how you calculated your tax.

However, it’s very important to always check these reports carefully. A calculator is only as good as the information you give it. You should verify that:

- All your transactions from every exchange and wallet are included.

- The cost basis methods used (like FIFO or Specific ID) match what you intended [^11, ^14].

- All your income from staking, mining, or airdrops is correctly listed.

Making sure everything is accurate helps ensure your tax report is correct and reduces your chances of an audit. For a deeper dive into organizing your crypto finances and preventing tax-time headaches, our 2026 Crypto Bookkeeping Guide is a great resource.

Staying updated on crypto tax rules is an ongoing task. For more step-by-step crypto education, safety tips, and clear guidance, consider exploring the free Clicks and Trades newsletter. It’s a simple way to keep up with the changing world of crypto and taxes.

Ready to feel more confident managing your crypto tax responsibilities?

Sign Up for helpful insights.

After getting your crypto records in order, the next big step is figuring out how much tax you might owe. This is where a good federal tax calculator becomes your best friend. In 2026, understanding your tax responsibilities for crypto is more important than ever because transactions like selling, trading, mining, or staking digital assets are typically taxable events [^4, ^6].

How a Federal Tax Calculator Helps Estimate Your Taxes

A federal tax calculator helps you see your full financial picture. Think of it this way: the government sees crypto just like other property you own [^1, ^9]. So, any profit you make from selling or trading crypto, or any income you get from things like staking or mining, adds to your total income for the year.

Here’s what a federal tax calculator does:

- Calculates Taxable Income: It takes all your income sources, including your crypto gains and income, and then subtracts things like deductions. The number left is your "taxable income."

- Applies Marginal Tax Rates: The calculator then shows you how different parts of your taxable income are taxed at different rates. For example, a small part of your income might be taxed at 10%, while a larger part might be taxed at 20% or more [^12]. The rate depends on how much you earn in total. If you hold crypto for less than a year, it’s often taxed like regular income, meaning higher rates for higher earners [^14].

- Estimates Tax Owed: Once it knows your taxable income and the right tax rates, the federal tax calculator can give you a clear idea of the total tax you’re likely to owe the government.

Making Estimated Tax Payments to Avoid Penalties

For many people with crypto, especially if you’re like a self-employed person earning income not tied to a regular job, you might need to make estimated tax payments. This means you pay your taxes little by little throughout the year, usually every three months, instead of waiting until the yearly tax deadline [^10]. This helps avoid a big surprise bill and penalties later.

To avoid penalties for not paying enough tax during the year, there are "safe harbor" rules [^13]. Generally, you won’t get a penalty if you pay at least 90% of the tax you’ll owe for the current year, or 100% of the tax you paid last year. If you have a higher income, it might be 110% of last year’s tax [^16]. A federal tax calculator can be a huge help here, as it allows you to estimate your tax for the year and plan those quarterly payments. Getting these payments right is key to avoiding issues with the tax office. For more on this, check out our guide on Crypto Taxes: The 2026 Guide to Avoiding Penalties and Audits.

Planning Your Cash Flow for Big Crypto Tax Bills

Imagine you have a really good year with crypto, maybe a big sale or lots of mining income. That’s exciting, but it can also mean a large tax bill you weren’t ready for. This is where cash-flow planning comes in handy.

Here are some tips:

- Set Money Aside: As soon as you have a big taxable event in crypto, try to set aside some money specifically for taxes. You can put it in a separate savings account so you don’t accidentally spend it.

- Use Your Calculator Often: Don’t just use your federal tax calculator once a year. Check it throughout the year, especially after significant crypto activity. This helps you see how much your tax bill might be growing.

- Be Ready for Surprises: Crypto markets can change fast. If you see a large gain, remember that a portion of that gain will likely go to taxes. Being prepared helps prevent stress.

Staying on top of your crypto taxes can seem like a lot. To get helpful updates, safety tips, and clear guidance in simple steps, you can explore the free Clicks and Trades newsletter. It’s a great way to keep learning about crypto and taxes in 2026.

Ready to feel more confident managing your crypto tax responsibilities?

Sign Up for helpful insights.

Even with a helpful federal tax calculator, it’s easy to make small mistakes that can cause big problems with your taxes. The tax office is getting better at watching crypto transactions in 2026, so it’s super important to get things right [^1]. Avoiding these common errors can help you stay out of trouble and keep your money where it belongs.

Common Mistakes Beginners Make with Federal Tax Calculators

Here are some typical mistakes people make when trying to calculate their crypto taxes:

- Missing Transactions: This is perhaps the biggest one. Many people forget to track every single crypto event. Think about selling, trading one crypto for another, using crypto to buy goods, or even getting crypto as payment for work (like for a self-employed person). All these are taxable events you must report [^2]. If you miss even a few, your federal tax calculator won’t give you the right answer. Good recordkeeping is key, as we talked about before.

- Incorrect Cost Basis: Your "cost basis" is simply how much you paid for your crypto, plus any fees. When you sell crypto, your profit is the selling price minus this cost basis. If you get this number wrong, your calculation of how much tax you owe will also be wrong. For example, if you think your cost was higher than it actually was, your federal tax calculator will show less profit and less tax, which could lead to an audit [^3].

- Mixing Up Income and Capital Gains: Not all crypto is taxed the same way. Crypto you earn from mining, staking, or getting paid in crypto is usually seen as regular income. But crypto you sell after buying it is often a capital gain or loss [^4]. These are taxed differently, so mixing them up means your "how to calculate tax" answer will be off.

- Ignoring Fees: Did you pay fees to buy, sell, or trade crypto? These fees can often be added to your cost basis or used to reduce your taxable income, which can lower your overall tax bill [^5]. Many beginners forget to include them when using their federal tax calculator.

How to Use Calculator Warnings and Avoid Audits

Many crypto tax tools and even some federal tax calculators can give you warnings if something looks off. Pay close attention to these! If a tool points out missing data or strange numbers, it’s telling you to double-check your work. The goal is to catch mistakes before the tax office does. Getting your crypto tax details right from the start means you’re much less likely to face an audit. The tax authorities are increasing their focus on crypto, so being prepared is important [^6].

To truly avoid tax chaos and stress, make sure you have solid records. You can learn more about this in our 2026 Crypto Bookkeeping Guide: Avoid Tax Chaos and Stress.

When to Consult a Tax Professional

A federal tax calculator is a fantastic tool for estimating your taxes, but it’s not always enough. If your crypto situation is complex, like if you’ve done many trades, used DeFi, or are a self-employed person earning a lot of crypto income, you might need a real expert. Tax professionals who specialize in crypto can help you navigate tricky rules and make sure everything is reported correctly. They can often spot things a calculator might miss, especially when it comes to specific deductions or how different types of crypto activities are taxed.

For bigger crypto tax questions or concerns about audits, it’s smart to talk to someone who knows the ins and outs. Check out our Crypto CPA Checklist: 5 Steps to Avoid IRS Penalties for guidance on when and how to find a good tax advisor.

Staying on top of your crypto taxes and avoiding mistakes is a big part of being a smart crypto owner. For more helpful updates, safety tips, and clear guidance in simple steps, explore the free Clicks and Trades newsletter. It’s a great way to keep learning about crypto and taxes in 2026.

Ready to feel more confident managing your crypto tax responsibilities? Sign Up for helpful insights.

After looking at common mistakes, it’s time to talk about how to use your federal tax calculator smartly and build good habits for the future. The trick is to use helpful tools, but also to double-check your work. Think of it like this: a calculator gives you a great estimate, but you’re still the boss who needs to make sure all the numbers are right.

To avoid tax surprises and problems, here are some simple steps:

- Get Your Records Straight: Before you even touch a federal tax calculator, make sure all your crypto trades and earnings are written down clearly. This means every time you buy, sell, trade, or earn crypto. Having all your transactions organized is the very first step to getting your taxes right. If you need help with this, our 2026 Crypto Bookkeeping Guide: Avoid Tax Chaos and Stress can show you how.

- Run a Test Estimate: Once your records are tidy, use a crypto tax tool or a federal tax calculator to get an idea of what you might owe. This is a good first look. It helps you see big picture numbers for your income and any capital gains or losses from your crypto. Remember, different types of crypto activities are taxed differently by the IRS [^7].

- Review and Fix Warnings: If your calculator or tax software gives you a warning about missing information or weird numbers, don’t ignore it. This is your chance to fix things before you send them to the tax office. Go back and check your data. Making sure everything is correct now can save you a lot of headache later.

- Save Your Records Safely: Once you feel good about your numbers, save reports from your crypto tax software or federal tax calculator. These reports should show how you calculated your tax owed. The IRS is watching crypto more closely in 2026, even introducing new forms like 1099-DA [^2], so having clear records is key if they ever have questions. These records can also help you use "safe harbor" rules to avoid penalties if you paid enough estimated taxes during the year [^3], [^4].

By using your federal tax calculator carefully and keeping good records, you can feel much more confident about your crypto taxes.

This helps you avoid fines and audits, which means less stress for you.

For more simple steps and clear advice on crypto and taxes, you can explore the free Clicks and Trades newsletter. It’s a friendly way to keep learning and stay on top of things in 2026.

Ready to feel more confident managing your crypto tax responsibilities? Sign Up for helpful insights.

Summary

This article explains why a federal tax calculator built for crypto can save time, reduce surprises, and help you stay compliant with U.S. tax rules in 2026. It walks through core functions—importing transactions, detecting taxable events, separating income from capital gains, and calculating cost basis using methods like FIFO or Specific Identification. The guide explains which crypto activities commonly create taxable events (sales, trades, spending, staking, mining, airdrops) and how DeFi and NFTs add complexity. You’ll learn practical steps to prepare your data, import via APIs or CSVs, fix common import mismatches, and run estimates for quarterly payments. The article also covers recordkeeping to build an audit-ready file, common mistakes that cause errors or delays, and when it’s wise to get a tax professional involved. After reading, you’ll know how to use a federal crypto tax calculator effectively and what checks to perform so your tax reports are accurate and defensible.

By

April 18, 2026