The 2026 Crypto Bookkeeping Guide: Avoid Tax Chaos and Stress

Introduction: Why Bookkeeping is Your First Line of Defense Against Crypto Tax Chaos

Picture this. It’s April 2026, and you’re finishing your taxes. You log into your crypto exchange and hit "download transaction history." What you get is a 300-page CSV file filled with codes, timestamps, and amounts you barely recognize. Your heart sinks. You have no idea what’s taxable, what’s a loss, or what you even did last July. This confusion is the direct path to a surprise tax bill, penalties, and serious stress.

This isn’t just a personal headache. It’s happening on a massive scale. Global authorities are intensely focused on closing the "tax gap," the difference between taxes owed and taxes paid. Initiatives like the American Families Plan Tax Compliance Agenda specifically target underreported income from new asset classes.

At the same time, regulators are cracking down on financial non-compliance, with reports highlighting billions in penalties for deficiencies in areas closely related to asset tracking. The message is clear: the era of flying blind with crypto is over.

That feeling of panic when you open your transaction history? That’s crypto tax chaos. It stems from one core failure: disorganized records. Without clear bookkeeping, you can’t possibly know your cost basis, your capital gains, or what to report. This disorganization breeds fear of the IRS, anxiety about making a mistake, and risks real non-compliance. It turns tax season from a routine task into a terrifying ordeal.

Here’s the good news. You can build a wall against this chaos. The solution isn’t a magic software or an expensive accountant you have to educate. It starts with a simple, powerful habit: personal business bookkeeping. Yes, bookkeeping. We often think of it as something only for business bookkeeping services, but the principles are your secret weapon. It’s the daily, weekly, or monthly practice of tracking what you buy, sell, earn, and spend in the crypto world.

Building this foundation does more than organize numbers. It builds confidence. When you have a clear record, you transform fear into understanding. You can have a productive conversation with a tax pro. You can spot errors before they become problems. You can finally see your true financial picture. This guide will show you how to set up that foundational system. Think of it as your crypto tax compass, pointing you toward calm and control.

For ongoing, step-by-step guidance to navigate this safely, subscribing to a trusted resource like the free Clicks and Trades newsletter can provide continuous education and safety tips.

Ready to turn chaos into clarity? It starts with your next step. Sign Up for clear guidance and take control of your crypto journey today.

The Foundation: What Crypto Bookkeeping Really Means (It’s More Than Just Tracking)

So, you know you need bookkeeping. But what does that actually mean for your crypto? It’s easy to think it’s just writing down what you bought and sold. That’s a start, but it’s not enough to protect you.

True bookkeeping is a system. It’s the disciplined process of recording, categorizing, and reconciling every financial move you make with digital assets. As defined by financial experts, bookkeeping is the foundational process of recording and organizing a business’s financial transactions. The core principles that guide professional business bookkeeping services, like consistency and accuracy, are exactly what you need for your crypto.

Let’s break down why crypto bookkeeping is different from tracking your regular bills or bank account.

Personal finance tracking asks: "How much did I spend? How much is left?"

Crypto bookkeeping asks: "What did I buy, at what price, on what date? When did I sell it, for how much, and what’s my gain or loss? Was that staking reward income? Was that NFT purchase an investment?"

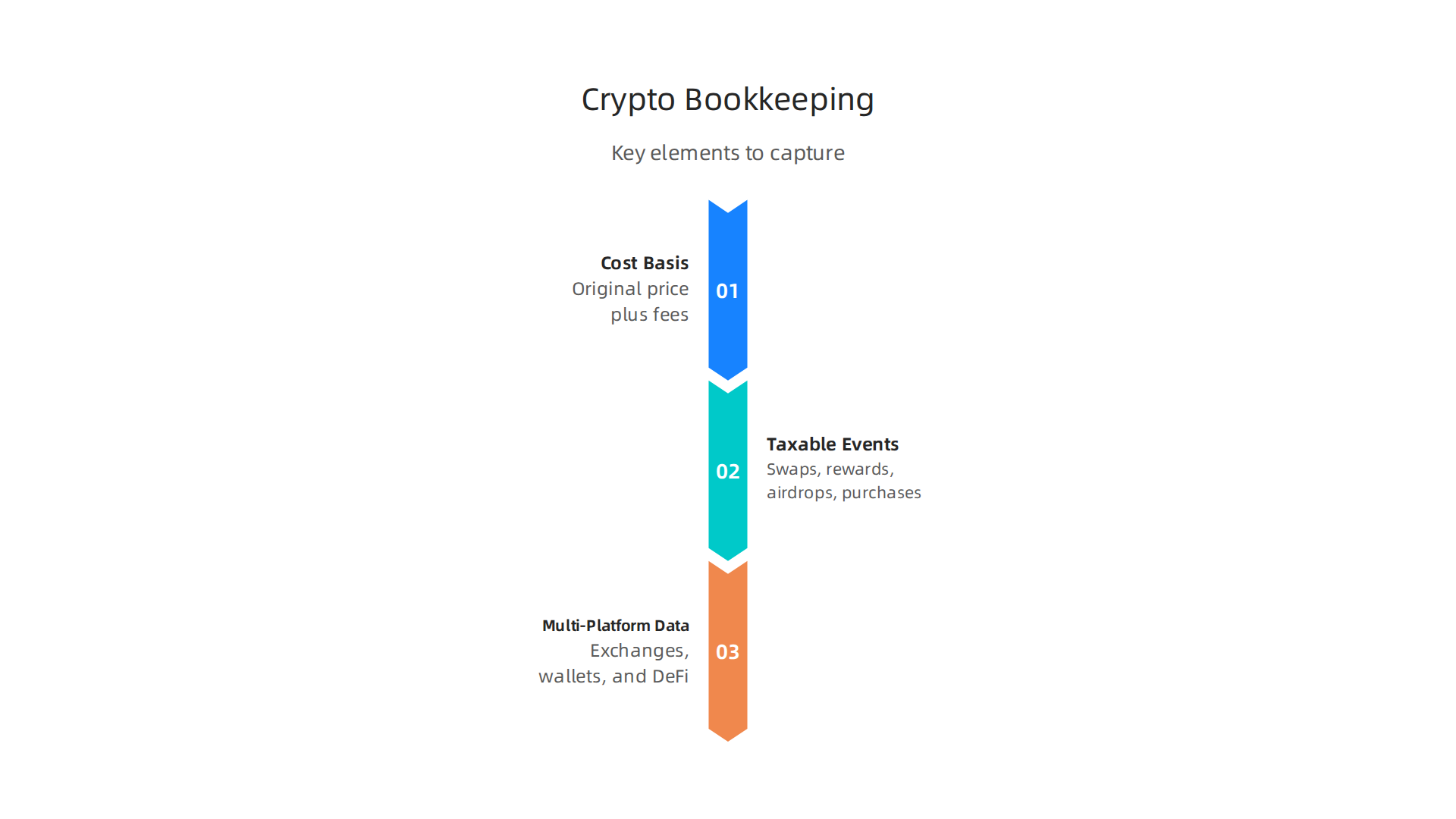

See the difference? Crypto adds layers of complexity that normal spending doesn’t have. Your system must capture:

- Cost Basis: The original price you paid for an asset, plus any fees. This is the single most important number for calculating your tax bill.

- Taxable Events: Not just selling for cash. Swapping one crypto for another, earning staking rewards, receiving an airdrop, or using crypto to buy a coffee can all be taxable events.

- Multi-Platform Data: Your transactions live across exchanges, wallets, and DeFi protocols. Good bookkeeping brings this scattered data into one clear, unified record.

This isn’t just busywork. This systematic approach directly attacks the core fears we talked about.

- It Ends Confusion: When every transaction is logged and categorized, you’re not staring at a cryptic CSV file. You’re reviewing a clear journal of your financial activity. You’ll know exactly what happened and when. For a deeper look at potential penalties for getting this wrong, our guide on avoiding crypto tax penalties and audits is essential reading.

- It Eradicates Fear: Uncertainty breeds anxiety. A solid ledger gives you proof. If you ever need to explain your activity to the IRS or a tax pro, you have a reliable, organized trail. This turns fear into preparedness.

- It Prevents Surprise Liabilities: You can’t be blindsided by a tax bill if you know your approximate capital gains throughout the year. Regular bookkeeping lets you see your financial picture in real time, so there are no nasty surprises in April.

Building this foundation might feel like a step reserved for a booming bookkeeping business, but the tools are accessible. Many people start with the best accounting software for small business, which is built on these same principles of double-entry bookkeeping and organized reporting. The key is to apply those principles to your unique crypto data.

Think of your crypto bookkeeping system as the source of truth. It’s the calm, organized center that all the chaos of the market flows into and gets sorted out. Getting this foundation right is the most important step you can take.

For ongoing, step-by-step support in building and maintaining this system, joining a community-focused resource like the free Clicks and Trades newsletter can provide continuous, clear guidance.

Ready to build your foundation of clarity? Start by getting the right guidance. Sign Up for clear, actionable insights to take control of your crypto bookkeeping today.

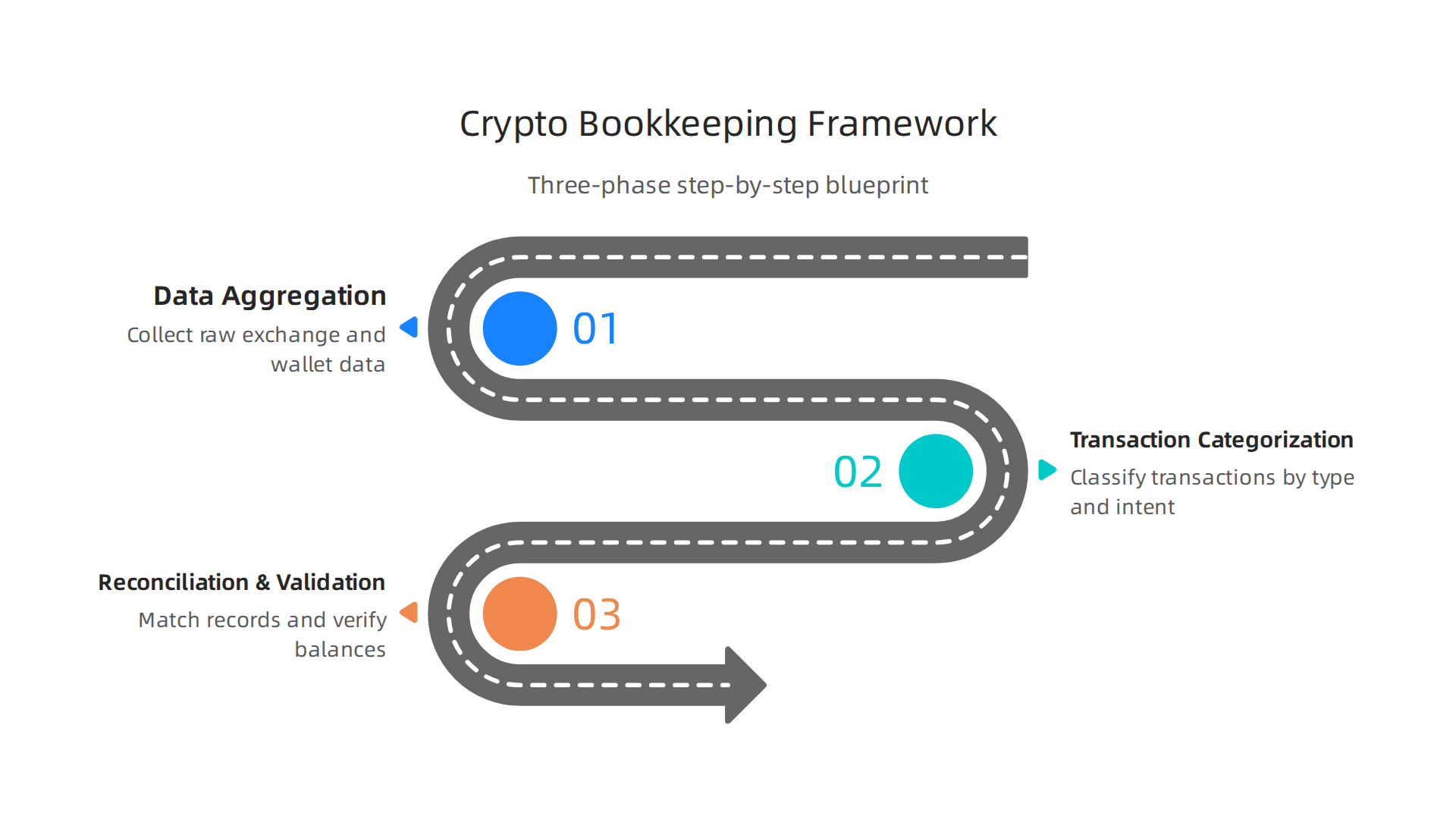

The Crypto Bookkeeping Framework: Your Step-by-Step Blueprint

Now that you understand the why behind crypto bookkeeping, let’s get into the how. A solid framework turns a vague idea into an actionable plan. Think of this as your personal blueprint for building a system of clarity, one block at a time.

Here is your three-phase framework to transform chaos into order.

Phase 1: Data Aggregation – Gather Everything, Everywhere

Your financial story is written across dozens of platforms. The first step is to collect every chapter. Data aggregation means systematically pulling all your transaction records into one place.

- Start with Centralized Exchanges (CEXs): Log into every exchange you use (Coinbase, Binance, Kraken, etc.). Download your complete transaction history, usually labeled as "Tax Documents," "Transaction History," or "Reports." Ensure you get the CSV or PDF file for the entire year. These reports are your primary source for trades and purchases.

- Move to Your Wallets: Don’t forget your self-custody wallets (like MetaMask, Phantom, or Ledger). You can’t download a statement, but you can find your public address. Use this address to pull a full transaction history from a blockchain explorer like Etherscan (for Ethereum) or Solscan (for Solana).

- Account for DeFi and Staking: This is where data gets tricky. Your activity on platforms like Uniswap, Aave, or Lido won’t appear on an exchange report. You’ll need to use your wallet address again to track swaps, liquidity provision, and rewards. Specialized crypto tax software can automate this, but manually, it starts with your wallet history.

- Don’t Forget the Extras: Include records from any peer-to-peer (P2P) trades, NFT marketplaces (like OpenSea), and records of any crypto income (from freelancing, staking rewards, or airdrops).

Why is this meticulous gathering so crucial? Because tax authorities are increasingly focused on digital asset compliance. A 2026 regulatory report from FINRA highlights the growing focus on "cyber-enabled fraud" and the importance of accurate financial records in this space. Having a complete dataset is your first line of defense.

Phase 2: Transaction Categorization – Label Every Move

Raw data is just a list of timestamps and amounts. Categorization is what gives it meaning. This is where you apply the rules of tax law to your activity. Each transaction type has different tax implications.

Here’s a simple guide to the essential labels:

| Transaction Type | What It Is | Why It Matters for Taxes |

|---|---|---|

| Buy | Acquiring crypto with fiat (like USD). | Establishes your initial cost basis. |

| Sell | Trading crypto for fiat. | A taxable event. You calculate gain/loss vs. your cost basis. |

| Trade/Swap | Exchanging one crypto for another (e.g., ETH for SOL). | This is a taxable event. The IRS treats it as selling one asset to buy another. |

| Income | Receiving crypto as payment, reward, or interest (staking, airdrops, earnings). | Taxable as ordinary income at its fair market value when received. |

| Transfer | Moving crypto between wallets you own. | Not a taxable event, but must be tracked to avoid confusing it with a sale. |

| Gift Sent/Received | Giving or getting crypto as a gift. | Has specific reporting rules and potential tax implications. |

As you label, you’ll identify your taxable events—the moments that trigger a tax calculation. The Global Digital Finance consortium notes that clear categorization is foundational for determining the correct "tax treatment of cryptoassets." Mislabeling here is a common source of errors and future headaches. For a detailed look at how these rules apply in specific situations, our guide on Virginia crypto tax rules provides a clear example.

Phase 3: Reconciliation & Validation – Check Your Work

This final phase separates good bookkeeping from great bookkeeping. Reconciliation means verifying that your internal records perfectly match your external account statements. Validation means checking for errors and ensuring nothing is missing.

- The Wallet Balance Check: Pick a date in the past. Your recorded bookkeeping should show exactly how much Bitcoin, Ethereum, or any other coin you held in each wallet on that date. Does it match your actual wallet balance from that time? If not, a transaction is missing or miscategorized.

- The Cost Basis Test: For a coin you sold, trace it back. Can you clearly identify which specific purchase it came from (FIFO is a common method)? Your calculated gain or loss should be clear and defensible.

- Look for "Ghost" Transactions: These are often small, easy-to-miss transfers or protocol interactions in DeFi that can generate unexpected tax consequences. Validating your records often means double-checking those complex wallet histories.

- Ensure Consistency: Are you using the same naming conventions and categories throughout the year? Consistency is a core principle of professional business bookkeeping services for a reason—it prevents confusion and errors.

This process of reconciliation is your quality control. It transforms your records from a "best guess" into a reliable source of truth. It’s the step that prepares your data for seamless use with the best accounting software for small business or for handing off confidently to a tax professional. In fact, following a structured checklist is the best way to ensure nothing slips through. Our crypto CPA checklist outlines the exact steps professionals use to validate crypto records.

Following this three-phase framework—Aggregate, Categorize, Reconcile—builds a system that withstands scrutiny. It turns the overwhelming into the manageable. For ongoing support through each phase, from finding your transactions to final validation, getting clear, step-by-step guidance is key. The free Clicks and Trades newsletter breaks down these processes into actionable tips delivered regularly.

Ready to implement your blueprint? Start with Phase 1 this week. Sign Up for straightforward guidance and build your system with confidence.

The Master Ledger: Creating Your Single Source of Truth

You’ve gathered your data and labeled your transactions. Now, where does it all live? This is the moment your bookkeeping moves from theory to practice. You need one central home for all your financial information. That home is called your master ledger.

A master ledger is your single source of truth. It’s where every transaction you’ve aggregated and categorized gets recorded in a standardized, consistent format. This isn’t just about being neat. It’s a core principle of professional bookkeeping. Following established rules, known as the principle of regularity, ensures your records are reliable and can be trusted for decision-making.

Without this central record, your data is scattered across dozens of downloaded reports. Finding a specific trade or calculating your annual gains becomes a nightmare. A well-kept ledger brings order, simplifies tax time, and is the backbone of any sound financial system, whether you’re managing a personal portfolio or using business bookkeeping services.

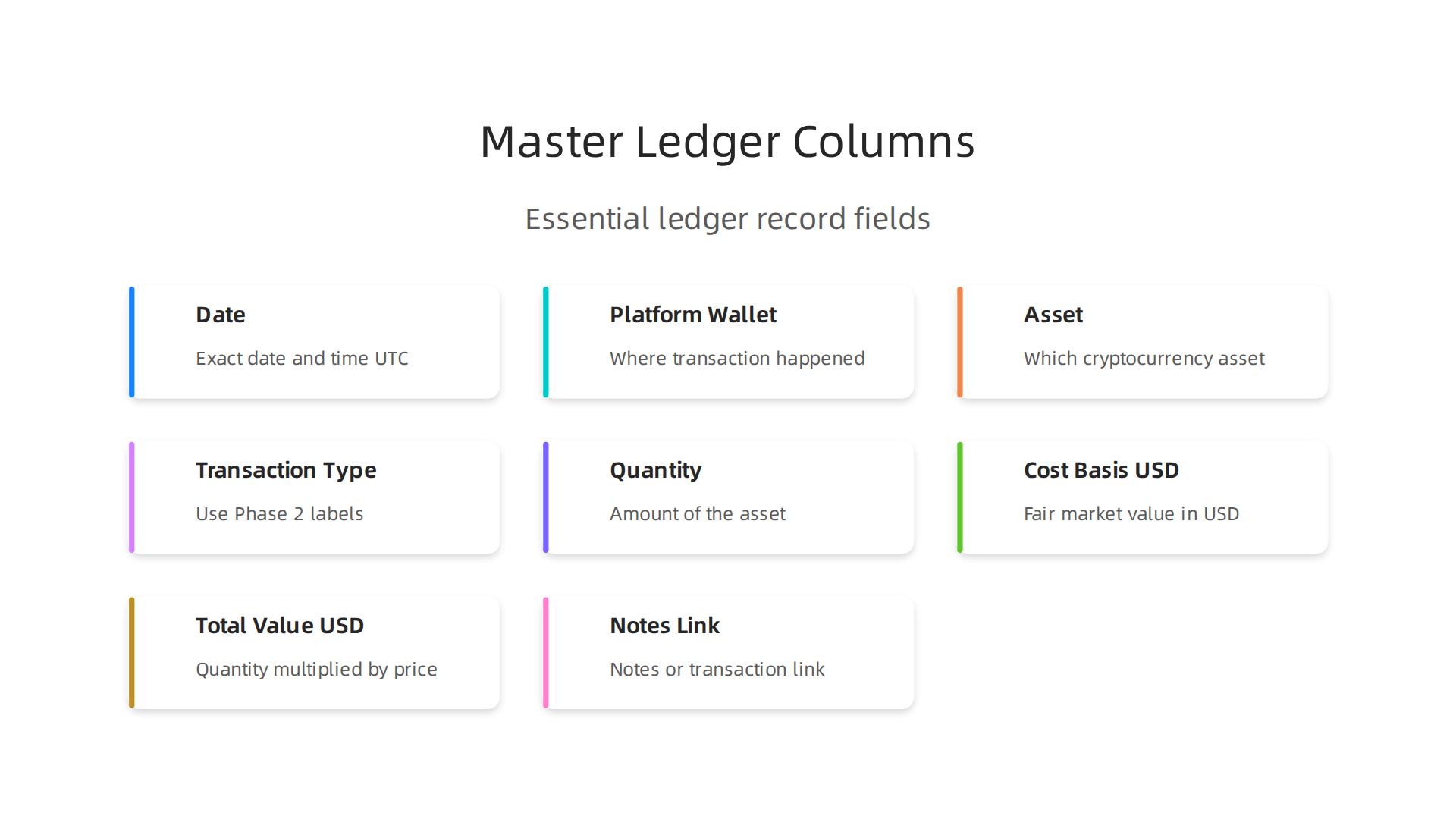

The Essential Columns Your Ledger Must Have

Your ledger can be a simple spreadsheet or within specialized software. The goal is consistency. Every single transaction gets its own row, and every row should contain the same set of information.

Here are the non-negotiable columns for your crypto master ledger:

| Column | What to Record | Why It’s Essential |

|---|---|---|

| Date | The exact date and time (UTC) of the transaction. | Establishes the timeline for tax calculations and capital gains holding periods. |

| Platform/Wallet | Where the transaction happened (e.g., Coinbase, MetaMask, Uniswap). | Tracks the source, crucial for reconciling with external statements. |

| Asset | The specific cryptocurrency involved (e.g., BTC, ETH, SOL). | Identifies what you’re tracking. |

| Transaction Type | Use your labels from Phase 2: Buy, Sell, Trade, Income, Transfer, etc. | Determines the tax treatment instantly. |

| Quantity | How much of the asset was involved (e.g., 0.5 ETH). | The base unit for all calculations. |

| Price/Cost Basis (USD) | The fair market value in USD at the time of the transaction. | This is the key to calculating your gains or losses. For buys, it’s what you paid. For income, it’s the value when received. |

| Total Value (USD) | Quantity multiplied by Price. | Shows the transaction’s total dollar value. |

| Notes/Link | A brief note (e.g., "Swapped for SOL on Uniswap") or a link to the blockchain transaction ID. | Provides context for future you or your tax preparer. |

Your Starter Template: Simple and Effective

You don’t need to start from scratch. Copy this basic structure into a spreadsheet and begin populating it with your categorized transactions.

Date, Platform, Asset, Transaction Type, Quantity, Price (USD), Total Value (USD), Notes

2026-10-26, Coinbase, BTC, Buy, 0.1, 65,000, 6,500, Initial purchase

2026-11-15, MetaMask, ETH, Trade, 0.5, 3,800, 1,900, Swapped for SOL on Uniswap, TxID: 0x123...

2026-12-05, Coinbase, BTC, Sell, 0.05, 70,000, 3,500, Partial sale

By maintaining this ledger, you are applying fundamental accounting principles that ensure consistency and accuracy. These principles, often called GAAP (Generally Accepted Accounting Principles), provide the framework that makes financial data clear and comparable. This disciplined approach turns your records into a powerful tool. It’s what prepares your data for seamless import into the best accounting software for small business or for a stress-free review with a professional.

Keeping this ledger updated is the habit that prevents year-end panic. For ongoing, step-by-step support in maintaining your financial clarity, the free Clicks and Trades newsletter breaks down these processes into actionable tips.

Start building your single source of truth today. Sign Up for clear guidance and take control of your crypto finances with confidence.

Navigating the Complexities: Bookkeeping for Staking, DeFi, NFTs & Other Advanced Activities

You’ve built your master ledger for simple buys and sells. That’s a huge step. But what happens when you step into the deeper end of the crypto pool? Activities like staking, providing liquidity in DeFi, or minting NFTs can turn your clean spreadsheet into a record-keeping puzzle overnight.

Here’s the thing. These activities are complex not because you can’t understand them, but because they create a flood of micro-transactions, generate new tokens out of thin air, and often have unclear cost basis rules. Each tiny action can be a taxable event. According to tax guides, activities like staking and DeFi participation can trigger income tax obligations, adding another layer to track.

The core principles of bookkeeping don’t change. Your goal is still to get every transaction into your ledger with a date, value, and clear label. But the how gets more specific. Let’s break down common scenarios.

Why Advanced Crypto Activities Are a Record-Keeping Challenge

Before we dive into examples, it’s helpful to know why this is hard. It usually comes down to three things:

- Multiple Micro-Transactions: A single DeFi interaction can involve several token approvals, swaps, and deposits across different protocols, all recorded on the blockchain separately.

- Unclear Cost Basis: When you receive new tokens from staking or liquidity mining, what’s their original value? For tax purposes, this is often the fair market value at the moment you gain control of them.

- New Token Creation: Earning governance tokens or LP (Liquidity Provider) tokens means you now have a new asset to track from $0 cost basis.

Getting this right is critical. A global report on crypto taxes highlights that crypto income, including from these advanced activities, is subject to corporate or income tax in many jurisdictions. Solid records are your first line of defense.

How to Record Common Advanced Scenarios

Use your master ledger’s columns, but apply these specific labels and notes. Here are concrete examples.

Scenario 1: Claiming Staking Rewards

- Transaction Type: Income

- What to Record: The day you claim or receive the rewards, you have taxable income. The IRS has confirmed that staking rewards are taxable as ordinary income when you receive them. Record the new tokens at their USD value the moment they hit your wallet.

- Example Ledger Entry:

Date: 2026-05-15 Platform: Lido Asset: stETH Transaction Type: Income Quantity: 0.05 Price (USD): 3,800 (value when received) Total Value (USD): 190 Notes: Staking rewards from 10 ETH staked on Lido.

Scenario 2: Providing Liquidity on a DEX (Like Uniswap)

This involves two steps:

- The Deposit: You swap two tokens (e.g., ETH and USDC) for a new LP token.

- Transaction Type: Trade (for each token you swap) and Transfer (for the receipt of the LP token).

- Notes: This is a disposal of your ETH and USDC for tax purposes. Your cost basis for the new LP token is the total combined USD value of the assets you deposited.

- Earning Fees: Over time, you earn trading fees, often in new tokens.

- Transaction Type: Income

- Notes: Record these as income at their value when you claim them.

Scenario 3: Minting or Buying an NFT

- For Minting: The gas fee (in ETH) to mint is your cost basis. Record the ETH spent as a Trade (ETH for the NFT). The NFT’s initial value is the USD value of that ETH plus any minting cost.

- For Buying: It’s a simple Trade (e.g., swapping ETH for the NFT). The NFT’s cost basis is the USD value of what you paid.

- Important: NFT taxation can be complex, as some may be treated as collectibles under tax rules, which can affect capital gains rates. Always document the transaction ID and a link to the NFT.

Practical Tips for When Data is Hard to Find

You won’t always have perfect data. Here’s what to do:

- Estimate Values: If you can’t find the exact historical price for a token at a specific hour, use a reliable price tracker for the day’s average or closing price. Document your source in your Notes column (e.g., "Used CoinGecko daily closing price for DATE").

- Document Assumptions: If you have to make an educated guess, write it down clearly. "Estimated value based on similar token price" is better than no note at all. This shows good faith effort if ever questioned.

- Use Your Categorization: Stick to your labels (Income, Trade, Transfer). Consistency will help you and any professional you work with make sense of it later. This disciplined approach is what separates basic note-taking from reliable business bookkeeping.

Managing this level of detail is where many seek help, either through specialized business bookkeeping services or by using the best accounting software for small business that can connect to blockchain wallets.

The key is to not let the complexity stop you from starting. Record what you can, note your assumptions, and keep building that single source of truth. For ongoing guidance on handling these complex crypto activities, the free Clicks and Trades newsletter offers clear, step-by-step advice to keep your finances organized.

Stay compliant and in control. Sign Up for straightforward tips and confidently navigate your entire crypto journey.

Tools of the Trade: From Manual Spreadsheets to Specialized Software

You have a solid grasp of what to record. Now, how should you record it? Your tool choice can mean the difference between a smooth tax season and a frantic, error-filled scramble. In 2026, you essentially have two paths: the hands-on control of a manual spreadsheet or the automated power of specialized crypto tax software.

Let’s break down the pros and cons of each to help you decide.

The Manual Spreadsheet: Control at a Cost

Starting with a spreadsheet, like Google Sheets or Excel, is where many begin. It’s familiar and feels like you have total control.

Pros:

- Total Control: You design the ledger exactly how you want it.

- Low Cost: It’s essentially free to start.

- Understanding: Manually entering data forces you to understand each transaction, which is great for learning.

Cons:

- Time-Consuming: Entering every trade, staking reward, and DeFi swap by hand takes hours.

- Prone to Error: One misplaced decimal or wrong formula can throw off your entire capital gains calculation.

- Hard to Scale: As your activity grows across multiple wallets and protocols, manual tracking becomes unsustainable.

A spreadsheet is a fantastic learning tool and may work for a handful of simple trades. But for serious activity, its limitations become clear fast. This is where dedicated tools step in.

Specialized Crypto Tax Software: Automation for Accuracy

Crypto tax software connects directly to your exchange accounts and wallet addresses via APIs. It imports your transactions, identifies what they are, calculates cost basis, and generates tax reports. As one 2026 review notes, this software "helps you take the pain out of manually calculating crypto taxes."

Pros:

- Saves Time: Automatically imports thousands of transactions in minutes.

- Improves Accuracy: Reduces human error in calculations and data entry.

- Handles Complexity: Good software can interpret staking, liquidity pools, and NFT mints, labeling them correctly.

- Creates Audit Trails: Provides a clear, organized report for your records or a tax professional.

Cons:

- Cost: Most platforms charge a fee, often based on your number of transactions.

- Learning Curve: You need to learn how to use the new platform.

- Import Imperfections: Not every protocol or wallet is supported perfectly, sometimes requiring manual adjustments.

Upgrading to software is often the smart move when you’re dealing with DeFi, frequent trading, or simply want peace of mind. It transforms bookkeeping from a chore into a streamlined process.

What to Look for in a Software Solution

Not all crypto tax platforms are created equal. If you decide to explore this route, here are key features to prioritize for your business bookkeeping needs:

| Feature | Why It Matters |

|---|---|

| Broad API & Wallet Connections | Can it import from all your exchanges, hot wallets, and even hardware wallets? The more integrations, the better. |

| Sophisticated DeFi & NFT Support | Does it correctly handle liquidity pool deposits, yield farming, and NFT transactions? This is crucial for modern crypto activity. |

| Clear Audit Trail | Does it show you the "why" behind every calculation, so you can explain it to an accountant or auditor? |

| Tax-Lot Accounting Methods | Does it let you choose FIFO, LIFO, or other methods to optimize your tax position? |

| Affordable Pricing | Does the cost fit your budget and scale reasonably with your transaction volume? |

Experts in 2026 consistently highlight platforms like Koinly, CoinTracking, and ZenLedger for their balance of features and support. For instance, independent reviews compare these tools across integrations and ease of use to help you find the best fit.

When Is It Time to Upgrade?

Think about upgrading from a DIY spreadsheet if:

- You have more than 50 transactions a year.

- You participate in staking, DeFi, or NFTs.

- You feel anxious about making a mistake on your taxes.

- You spend more time organizing data than analyzing your investments.

Using the best accounting software for small business ventures into crypto is an investment in your compliance and sanity. It ensures your business bookkeeping services, whether you handle them yourself or hire out, start with clean, reliable data.

Choosing the right tool empowers you. It turns record-keeping from a source of stress into a simple, automated background task. This lets you focus on what matters: making informed decisions and growing your portfolio.

For ongoing, plain-English guidance on choosing tools and managing crypto finances, many find value in a dedicated resource like the free Clicks and Trades newsletter. It offers step-by-step advice to keep you organized and confident. To stay ahead of the curve with straightforward tips, you can Sign Up today.

Common Crypto Bookkeeping Pitfalls (And How to Avoid Them)

You’ve chosen your tools, whether it’s a trusty spreadsheet or powerful software. But even the best setup can’t save you from certain human errors. These bookkeeping mistakes are surprisingly common, and they can turn a simple tax filing into a stressful, expensive ordeal.

Here are three of the biggest pitfalls in crypto business bookkeeping and exactly how to steer clear of them.

Pitfall 1: Ignoring Small Transactions & Gas Fees

It’s easy to think, "It’s just a few dollars, it doesn’t matter." This is a dangerous mindset. Every trade, every transfer, and every network fee (gas) changes your cost basis. Over hundreds of transactions, these small amounts add up to a significant miscalculation.

If you ignore fees, you’re incorrectly stating how much you spent to acquire an asset. This leads to wrong profit calculations. You could end up overpaying on taxes by thousands. As experts note, overlooking cost basis is one of the most frequent triggers for IRS scrutiny.

How to Avoid It:

- Record Everything: Log every transaction, no matter how small. Treat gas fees as part of the cost of your transaction.

- Use Software That Captures Fees: Choose a platform that automatically imports and categorizes network fees. This is a key feature of the best accounting software for small business crypto needs.

- Review Imported Data: Don’t blindly trust imports. Periodically check that your software has captured all small transfers and fees correctly.

Pitfall 2: Failing to Reconcile Across Platforms

You trade on Coinbase, swap on Uniswap, and hold NFTs in MetaMask. If you only look at one account at a time, you’re missing the full picture. A transfer from an exchange to your wallet might look like a disposal on the exchange records but won’t show as an acquisition in your wallet history if you don’t connect them. This causes either missing or double-counted transactions.

How to Avoid It:

- Connect All Wallets and Exchanges: Use your software’s API to link every platform you use for a unified view.

- Perform Regular Reconciliation: Monthly or quarterly, ensure the flow of assets between your accounts makes sense. Your total assets should be traceable from one wallet to another.

- Understand Wallet Transfers: Remember, sending crypto from Exchange A to Wallet B is a taxable disposal event on Exchange A. Proper bookkeeping tracks this movement correctly to avoid errors.

Pitfall 3: Poor Documentation of Non-Exchange Activity

Centralized exchanges provide some records. The real bookkeeping black hole is your direct wallet activity. Sending crypto to a friend, donating to a project, providing liquidity in a DeFi pool, or receiving an airdrop directly to your wallet creates taxable events that leave no paper trail with a third party. If you don’t document these yourself, they vanish from your financial history.

How to Avoid It:

- Manually Log "Invisible" Transactions: Immediately record any direct wallet interactions. Note the date, amount, purpose, and counterparty address.

- Use a Wallet Tracker: Some tax tools can read your public wallet address and help identify these transactions, but you may need to add context.

- Keep External Proof: Save screenshots, Discord messages, or receipts that explain the transaction’s purpose. This creates an audit trail. For more on building a solid defense, see our guide on avoiding penalties and audits.

Solid business bookkeeping services, whether you do them yourself or hire help, are built on complete and accurate data. Avoiding these three pitfalls protects you from costly corrections and gives you peace of mind.

For ongoing, plain-English guidance that helps you spot and fix these common errors, many find value in a dedicated resource like the free Clicks and Trades newsletter. It delivers step-by-step advice to keep your crypto finances organized and compliant. To get clear tips sent directly to you, you can Sign Up today.

From Bookkeeping to Filing: Bridging the Gap with Confidence

You’ve avoided the big bookkeeping pitfalls. Your records are clean, complete, and reconciled. Now what? The true reward for your diligent bookkeeping is a smooth, stress-free transition to filing your taxes. Think of your organized ledger as the raw material. The tax forms are the finished product. This section is about that final, confident assembly.

Good records don’t just make filing easier. They transform a confusing chore into a straightforward process and build an unshakable defense if questions arise.

Your Records Become Your Tax Forms

Modern crypto tax software is the bridge here. When you connect your unified transaction history, these platforms automatically calculate your capital gains and losses, then map them directly to the IRS forms you need, primarily Form 8949 and Schedule D.

This is where using the best accounting software for small business crypto operations pays off. It reads your well-kept ledger—where every gas fee and transfer is logged—and performs the complex math for you. According to a recent industry analysis, having organized data is the single biggest factor in user success with tax compliance tools. You are no longer manually sifting through hundreds of trades. Your business bookkeeping services, whether self-run or professional, have done the heavy lifting.

Your Peace of Mind in an Audit

An audit is about proof, not panic. If the IRS has questions, your comprehensive records are your answer. Auditors want to see a clear paper trail from acquisition to disposal.

Can you explain that large transfer to an external wallet? Your bookkeeping notes have the date, amount, and purpose. Can you verify your cost basis for a specific coin? Your ledger shows the original purchase plus all associated fees. This level of detail turns a potentially adversarial process into a simple verification. For a deeper look at building this defensive documentation, review our guide on the crypto CPA checklist to avoid IRS penalties.

The Final Review: What to Check Before You File

Before you submit, take one last pass. This final review catches the errors that slip through automated imports. Here’s a simple checklist:

- Verify Gross Proceeds vs. Cost Basis: Ensure the totals on your generated Form 8949 make sense. Do the "proceeds" and "cost" columns roughly align with your trading activity?

- Spot-Check Complex Transactions: Manually review a few DeFi swaps, NFT purchases, or staking rewards entries. Did the software categorize them correctly?

- Reconcile to Year-End Balances: Do the final holdings in your tax report match your actual wallet and exchange balances as of December 31?

- Review for Missing Wallets: Double-check that you connected every single wallet, especially those used for direct peer-to-peer transactions.

Completing this review is the last step in your bookkeeping journey. It ensures the confidence you built by keeping good records translates directly into confidence when you file.

The world of crypto tax rules continues to evolve, with experts tracking significant developments for 2026 and beyond. Staying informed is key to maintaining this confidence year after year. For ongoing, plain-English guidance that helps you manage these changes, many find value in a dedicated resource like the free Clicks and Trades newsletter. It delivers step-by-step advice to keep your crypto finances organized and compliant. To get clear tips sent directly to you, you can Sign Up today.

Summary

This article explains why disciplined bookkeeping is the best defense against crypto tax chaos and shows a practical system you can implement today. It defines crypto bookkeeping as a repeatable process—aggregate your scattered data, categorize every transaction by tax treatment, and reconcile records into a single master ledger. The guide walks through a three-phase framework (data aggregation, transaction categorization, reconciliation), details the essential ledger columns, and explains how to handle advanced activities like staking, DeFi, and NFTs. It compares manual spreadsheets versus specialized crypto tax software, lists common pitfalls to avoid, and gives a final checklist to prepare your records for filing or an audit. After reading, you’ll know what to record, how to organize it, which tools to consider, and how to produce defensible tax reports that reduce surprises and stress.

By

April 17, 2026